The Cost of Business in Singapore Compared With Hong Kong, China

Op/Ed by Chris Devonshire-Ellis

Op/Ed by Chris Devonshire-Ellis

Part Seven in our series comparing ASEAN business costs with China

Singapore is the de facto financial and services hub for ASEAN, and as a city state with such a remit it is more pertinent to compare the dynamics of Singapore with Hong Kong rather than China as a whole. The two cities compete with each other – yet how do they stack up when compared?

In fact, since Hong Kong’s return to mainland China in 1997, its positioning as a services hub has retrenched from Asia to being almost exclusively the gateway to mainland China, and a bridge between China and Taiwan. Singapore meanwhile has forged ahead with its ASEAN ties, and has become a regional hub for the bloc, meaning that today a clear distinction can be drawn between the markets they serve. Although a little simplistic, the general rule of thumb that Hong Kong services the mainland, and Singapore ASEAN, contains much truth, and particularly so when one realizes that Hong Kong is not included in the China-ASEAN Free Trade Agreement although negotiations are now underway.

The two cities have differed in their treatment of immigrant talent over the past 15 years as well, Hong Kong has become increasingly Sinicized, leading to the loss of some indigenous culture and the creation of some tensions between locals and mainland immigrants and tourists, while Singapore has been rather more selective and has made academic needs as well as wealth a prerequisite for immigration. While the Singaporean government has been criticized for being authoritarian, the city now generally upholds higher standards of living and maintenance than Hong Kong, where public roads are in danger of becoming in serious need of maintenance. The irony of Beijing being seen elsewhere as authoritarian seems lost on many Hong Kongers when it comes to comparisons with Singapore.

![]() RELATED: Dezan Shira & Associates’ Tax and Compliance Services

RELATED: Dezan Shira & Associates’ Tax and Compliance Services

However, the evolution of China, especially as it flexes its economic power throughout Asia, means that Hong Kong and Singapore also compete for similar business. Both cities, for example, are RMB trading hubs and both attract mainland Chinese companies for investment. So from a business cost and trade perspective, how do they stack up?

Hong Kong Trade

Exported Products: Gold (37%), Telephones (5.1%), Jewellery (3.4%), Silver (2.2%), and Scrap Copper (1.9%)

Imported Products: Gold (9.9%), Telephones (6.4%), Computers (5.8%), Integrated Circuits (5.6%), and Broadcasting Equipment (4.9%)

Services Industry as % of Total Exports: 30%

These figures show Hong Kong’s deep involvement in the jewelry trade, with basic materials being reworked into designs mainly for the China market, as well as being a transshipment hub for electrical products also ultimately destined for the mainland China market. Top quality products are often available in Hong Kong and at lower prices than in China, where a more stringent regulatory regime, especially concerning communications equipment is in place, as well as luxury tax surcharges on imported items. This encourages mainland Chinese entrepreneurs to purchase products in the city and return with them to China as personal items which are then resold. This round tripping to reduce mainland tax burdens on specific quality products has now become a major ‘tourism’ industry statistic in Hong Kong. However, given the very low value attached to jewelry workmanship it is arguable whether Hong Kong is adding any real value in its processing industry.

![]() RELATED: The Cost of Business in Malaysia Compared With China

RELATED: The Cost of Business in Malaysia Compared With China

As Hong Kong manufacturing and processing continues to decline as a result of moving to mainland China, the services industry has been growing. This encompasses mainly trade support services such as advertising, fairs, and marketing in addition in financial services. Much of these are aimed at mainland China. It is also worth noting that many of the businesses registered as “manufacturing” entities in Hong Kong instead act as holding companies or service operations for mainland China subsidiaries, meaning that the services ratio of export trade in Hong Kong is probably higher than the official estimates shown.

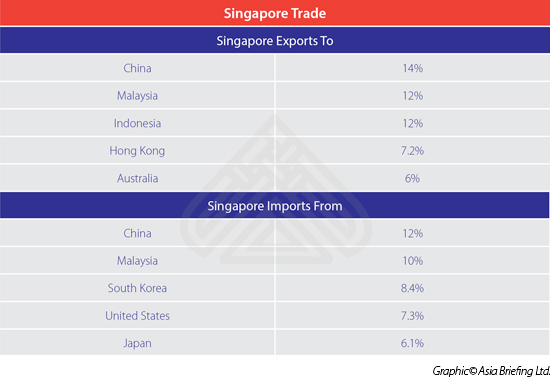

Singapore Trade

Exported Products: Refined Petroleum (28%), Integrated Circuits (7.9%), Computers (4.3%), Oxygen Amino Compounds (3.2%), and Packaged Medicaments (2.1%)

Exported Products: Refined Petroleum (28%), Integrated Circuits (7.9%), Computers (4.3%), Oxygen Amino Compounds (3.2%), and Packaged Medicaments (2.1%)

Imported Products: Refined Petroleum (23%), Crude Petroleum (12%), Integrated Circuits (6.5%), Computers (2.7%), and Petroleum Gas (2.0%)

Services Industry as Total of Exports: 72%

By contrast, Singapore has developed a value-added petrochemicals industry as is shown in its figures, in addition to developing IT and pharmaceutical repackaging (India generics, some Chinese TCM) with a wider remit than Hong Kong’s market base and less dependence upon China. It has also been rather more driven in its pursuit of developing a services industry than Hong Kong, with financial and business services dominating, followed by IT, transportation and communications.

Singapore has also been extremely active in signing bilateral Double Tax Treaties, with nearly 100 in existence. It also has a free trade agreement with the United States. In contrast, Hong Kong’s policy as concerns DTA and other agreements has been patchy over the past few years. Beijing is responsible for Hong Kong’s foreign affairs, yet it has not included Hong Kong as a territory under some of its most important agreements (such as the ASEAN FTA). Consequently there is some confusion about treaty status concerning the territory. Hong Kong does have a “Closer Economic Partnership Agreement“

(CEPA) with China, however the qualifying period to access this can be seven years. Hong Kong also has about 30 DTA agreements in place – about a third of that agreed by Singapore. In comparison, Hong Kong’s position appears somewhat confused, neither fully part of China’s own bilateral agreements yet unable to proceed unilaterally without Beijing’s approval.

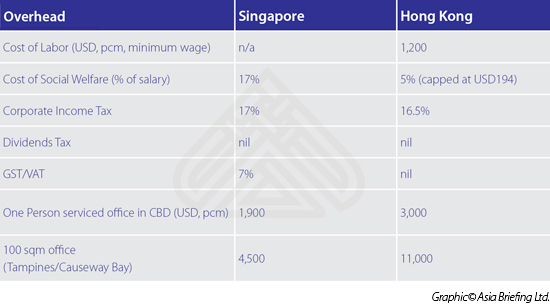

Meanwhile we can compare the operational costs in each city as follows:

Hong Kong remains a service center and gateway for China, however, in my view there are serious questions to be asked concerning existing policies as concerns its positioning as a regional hub, and especially so when compared with Singapore. Hong Kong appears not to have been provided with any visionary plan to take it forward as an Asian service center, other than loose plans to integrate it into the Pearl River Delta and use it as a hub for generating investment capital for Chinese companies listing on its bourse. Meanwhile, property prices have rocketed, pushing the cost of office rentals extremely high, while much of the China tourism figures appears to have been taken up with parallel trading rather than attempts to offer a bona fide high value visit experience. In short, the territory has been mismanaged.

Hong Kong remains a service center and gateway for China, however, in my view there are serious questions to be asked concerning existing policies as concerns its positioning as a regional hub, and especially so when compared with Singapore. Hong Kong appears not to have been provided with any visionary plan to take it forward as an Asian service center, other than loose plans to integrate it into the Pearl River Delta and use it as a hub for generating investment capital for Chinese companies listing on its bourse. Meanwhile, property prices have rocketed, pushing the cost of office rentals extremely high, while much of the China tourism figures appears to have been taken up with parallel trading rather than attempts to offer a bona fide high value visit experience. In short, the territory has been mismanaged.

Costs are already forcing many back office operations, and Hong Kong residents into nearby Guangdong cities such as Shenzhen, and it remains unclear what the city’s actual function is really intended to be. For now, it remains a good location from which to base a trading company dealing with China, due to its wealth of talent and proximity to the mainland. And the services sector in Hong Kong largely remains world class in this regard. Whether it can maintain this with the rise of Shenzhen’s and Shanghai’s lower operational costs and existing compliance with mainland Chinese laws will depend on future customs regulations. Beijing’s intentions and the anticipated development of China itself make Hong Kong’s future role questionable, especially as the city possesses no other added value industry. This makes Hong Kong a China play only, with the potential for the services industry to migrate directly to China. This process has already begun and will continue unless the Central Government can provide Hong Kong with a specific, defined, and planned role for the future.

![]() RELATED: The Cost of Business in the Philippines Compared With China

RELATED: The Cost of Business in the Philippines Compared With China

Singapore meanwhile has positioned itself as the gateway to Asia, and followed this through with very specific plans and a long-term strategy. Whereas Hong Kong has embraced China, Singapore has embraced a rather more diverse Asia, and in doing so has made itself a melting pot of pan-Asian languages and culture, and especially so within ASEAN, something Hong Kong has singularly failed to do. Singapore has also invested in a true added value industry by importing crude and other petroleum and gas products from ASEAN neighbors, and Indonesia particularly, then processing these for export. Hong Kong has not achieved this.

Meanwhile, the two cities remain competitive in terms of economic environment, such as tax rates and so on, although operational costs such as rental in Hong Kong are double the price of Singapore. But it is Singapore that has developed as a true Asian regional hub, leaving Hong Kong to deal almost exclusively now with China, and far from certain about its own destiny.

In conclusion, Hong Kong despite its issues, currently remains the best services hub for dealing with mainland China, although Shenzhen may now start to be considered as a viable alternative. Singapore though is a superior services hub for dealing with ASEAN, with the clinching argument for either being proximity of markets, but also language capabilities and the wealth of local experience towards the respective target markets possessed uniquely in each.

|

Links to the other articles in this series are as follows:

|

||||||||||

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email asean@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight. |

![]()

Tax, Accounting, and Audit in Vietnam 2014-2015

Tax, Accounting, and Audit in Vietnam 2014-2015

The first edition of Tax, Accounting, and Audit in Vietnam, published in 2014, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in Vietnam, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in Vietnam in order to effectively manage and strategically plan their Vietnam operations.

An Introduction to Tax Treaties Throughout Asia

An Introduction to Tax Treaties Throughout Asia

In this issue of Asia Briefing Magazine, we take a look at the various types of trade and tax treaties that exist between Asian nations. These include bilateral investment treaties, double tax treaties and free trade agreements – all of which directly affect businesses operating in Asia.

The 2015 Asia Tax Comparator

In this issue, we compare and contrast the most relevant tax laws applicable for businesses with a presence in Asia. We analyze the different tax rates of 13 jurisdictions in the region, including India, China, Hong Kong, and the 10 member states of ASEAN. We also take a look at some of the most important compliance issues that businesses should be aware of, and conclude by discussing some of the most important tax and finance concerns companies will face when entering Asia.

- Previous Article 26th ASEAN Summit sees Progress on AEC and FTA with Hong Kong

- Next Article Indonesia’s Economy Struggles to find its Footing