The Philippines’ New Tax Reform Package Approved

By Dezan Shira & Associates

Editor: Vasundhara Rastogi

On December 19, 2017, the Philippines’ much awaited tax reform package or Tax Reform for Acceleration and Inclusion (TRAIN) was signed into law, paving the way for a simpler and fairer tax regime in the country. The revised law provides for personal income tax cuts and revises several other decade-old tax provisions that will have important implications for taxpayers and businesses in the Philippines.

In this article, we highlight the key changes introduced in the new Act.

Tax exemptions

- Personal Income Tax exemption for lowest earners

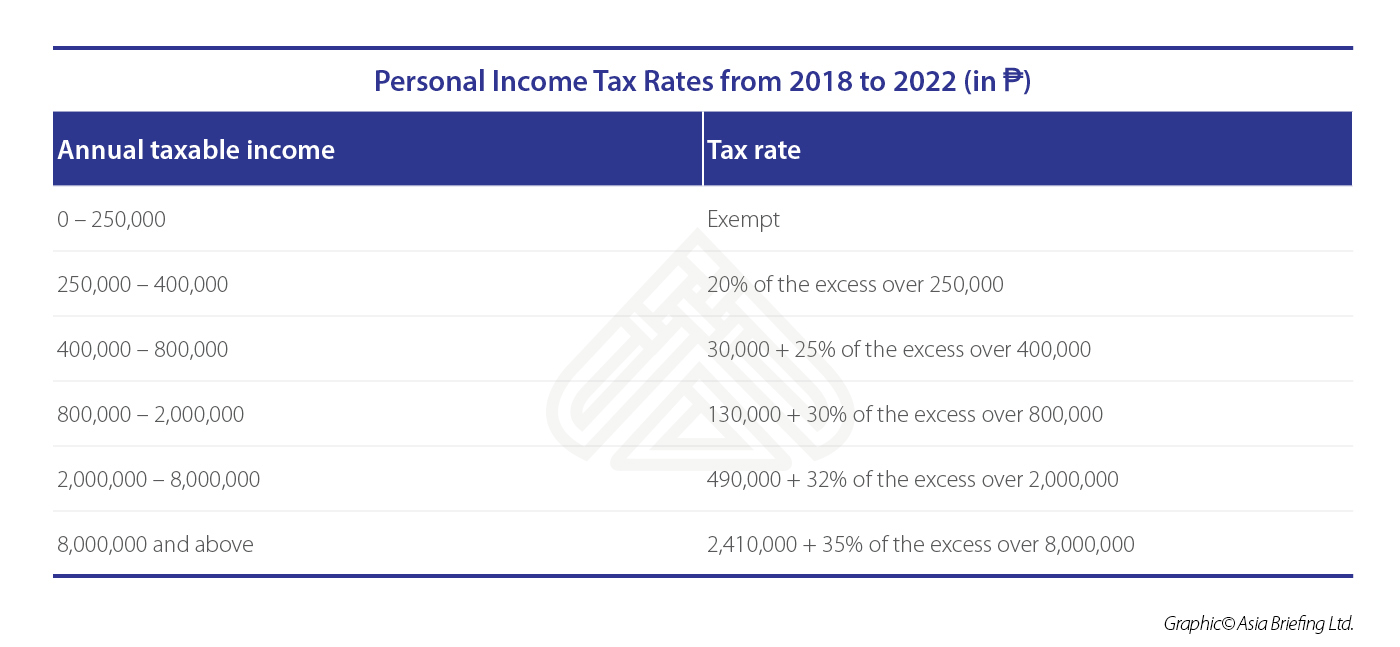

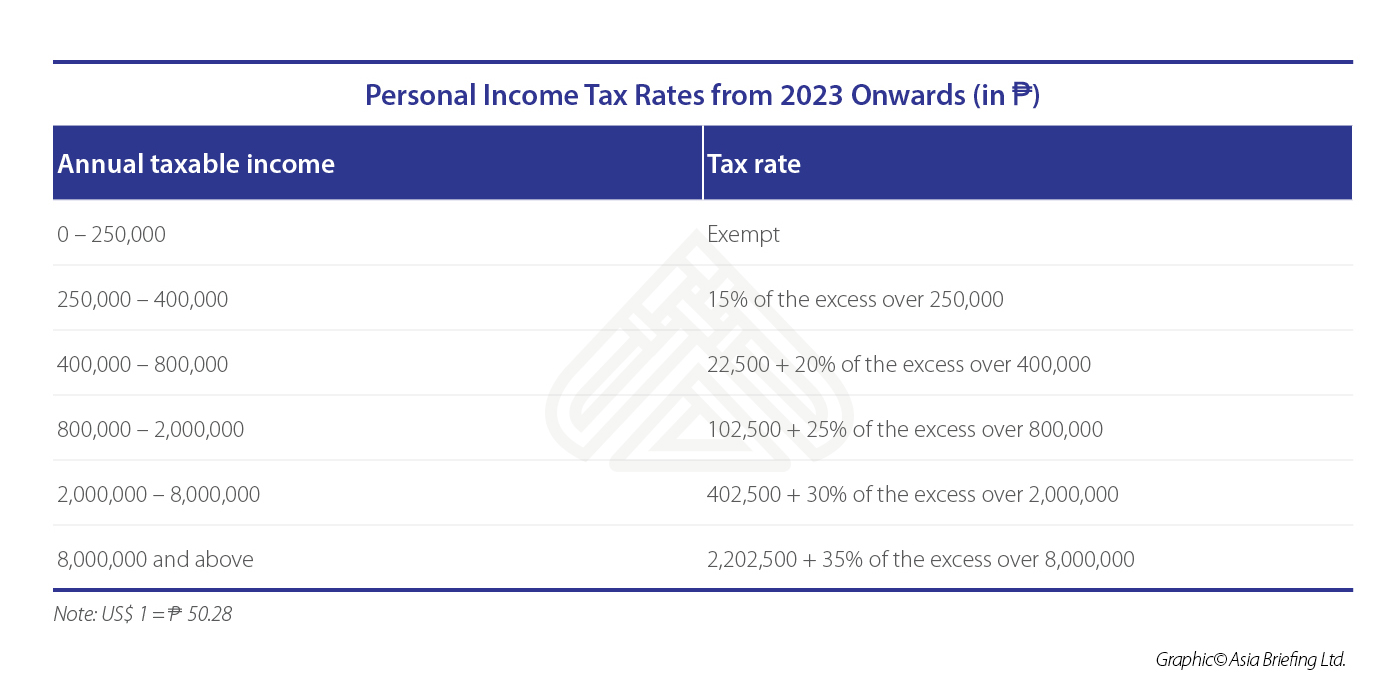

TRAIN exempts those earning an annual income of up to ₱250,000 (US$4,975) from Personal Income Tax (PIT), and raises the tax exemption for 13th-month pay and other bonuses to ₱90,000 (US$1,791). In addition, it lowers income tax rates for those earning up to ₱8 million (US$159,200). After 2022, the income tax rates will further be reduced for all taxpayers, except those earning an annual income above ₱8 million.

![]() RELATED: Tax Services from Dezan Shira & Associates

RELATED: Tax Services from Dezan Shira & Associates

The revised PIT rates are shown in the table below.

- VAT exemption

Further, the new tax law increases the value-added tax (VAT) threshold from ₱1.9 million (US$37,810) to ₱3 million (US$59,700), to encourage economic growth and job creation in the Philippines. As a result of this change, small businesses with annual sales of ₱3 million or below will now be exempted from the VAT.

Other VAT exempt sectors and individuals include senior citizens, cooperatives, tourist enterprises, socialized housing valued at ₱450,000 (US$8,955) and below, BPOs located in special economic zones, and agricultural products among others.

RELATED: Entering the Philippine Market: Comparing Models

RELATED: Entering the Philippine Market: Comparing Models

Additional taxes

To offset the revenue lost due to exemptions in PIT, the government has increased levies on petroleum products, sugar-sweetened beverages, automobiles, and coal.

- Excise taxes on automobiles, and fuel

Cars priced up to ₱1 million (US$19,900) will be charged 10 percent tax. Those valued at more than ₱1 million will be taxed at a 20 percent rate, while cars priced above ₱4 million (US$79,600) will be taxed at 50 percent.

At present, there is no excise tax levied on diesel. However, from January 1, 2018, an excise tax will be levied on diesel at ₱2.5 (US$0.05) per liter. This will be raised to ₱4.50 (US$0.09) in 2019, and to ₱6 (US$0.12) in 2020. Similarly, liquid petroleum gas (LPG) will be taxed at ₱1 (US$0.02) per kilogram in 2018, at ₱2 (US$0.04) in the following year and at ₱3 (US$0.06) in 2020.

TRAIN also aims to increase excise tax on coal from ₱10 (US$0.20) per metric ton to ₱150 (US$3) per metric ton over a period of three years. The increase will be in increments of ₱50 (US$1), starting from ₱50 in 2018.

Other variants of fuel such as kerosene, gasoline, lubricating oils, and greases will also be charged additional taxes.

- Tax on sugar-sweetened beverages

Sugar-sweetened beverages such as powdered juice, energy and sports drinks, soft drinks, cereal and other grain beverages will be taxed at a higher rate of between ₱6 (US$0.12) and ₱12 (US$0.24) per liter depending on the contents and quantity of sweetener used.

All milk and coffee products, however, are exempted from the levy. Other exempted drinks include 100 percent natural fruit and vegetable juices, meal replacements, as well as medically-indicated beverages.

Estate tax and donor’s tax

Previously, an estate worth ₱200,000 (US$3,980) and above was taxed between 5 and 20 percent of the net value of the estate. The revised tax law sets a flat rate of 6 percent for estate tax, as well as for donations and gifts valued ₱100,000 (US$1,990) annually, or above.

Family homes valued up to ₱10 million (US$199,000) are also exempted from estate tax. Earlier, the maximum threshold value for VAT exemption was limited to ₱1 million (US$19,900).

|

![]()

Dezan Shira & Associates Brochure

Dezan Shira & Associates Brochure

Dezan Shira & Associates is a pan-Asia, multi-disciplinary professional services firm, providing legal, tax and operational advisory to international corporate investors. Operational throughout China, ASEAN and India, our mission is to guide foreign companies through Asia’s complex regulatory environment and assist them with all aspects of establishing, maintaining and growing their business operations in the region. This brochure provides an overview of the services and expertise Dezan Shira & Associates can provide.

An Introduction to Doing Business in ASEAN 2017

An Introduction to Doing Business in ASEAN 2017

An Introduction to Doing Business in ASEAN 2017 introduces the fundamentals of investing in the 10-nation ASEAN bloc, concentrating on economics, trade, corporate establishment, and taxation. We also include the latest development news for each country, with the intent to provide an executive assessment of the varying component parts of ASEAN, assessing each member state and providing the most up-to-date economic and demographic data on each.

ASEAN’s FTAs and Opportunities for Foreign Businesses

ASEAN’s FTAs and Opportunities for Foreign Businesses

In this issue, we provide an introduction to some of ASEAN’s FTAs and how foreign investors and exporters can maximize opportunities in this dynamic region. We also discuss the salient features of each FTA and the overall benefits they offer. We then discuss the Rules of Origin criteria associated with each FTA that foreign businesses need to be aware of. Finally, we analyze the growing opportunities for investors looking to set up alternative production bases within ASEAN.

- Previous Article China SOEs Bid On Philippines Clark International Airport Development

- Next Article Singapore’s Investment Outlook for 2018