Incentives for Doing Business in Indonesia

Indonesia has enhanced and improved the incentives offered to businesses in a bid to spur foreign and domestic investments into the country. These incentives include long-term tax reductions for major investments, no import/excise duties, and a simplified immigration process.

Indonesia has in recent years enhanced and improved the incentives offered to businesses in a bid to spur foreign and domestic investments into the country. This was apparent when Government Regulation in Lieu of Law No. 2 Year 2022 was launched as possibly one of the most significant economic reforms since 1998. The Law removes more than 70 labor, tax, and other key laws to reduce bureaucratic inefficiencies, simplify business licensing requirements, and liberalize more industries for foreign investors.

Tax incentives for investments in priority sectors

Companies that invest a certain amount in one of the 246 priority business lines will be afforded fiscal and non-fiscal incentives.

Fiscal incentives include a 50 percent corporate income tax reduction for investments between 100 billion rupiah (US$6.6 million) and 500 billion rupiah (US$33.3 million) for a period of five years and a 100 percent CIT reduction for investments over 500 billion rupiah (US$33.3 million) for a period between five and 20 years.

In addition, there are tax allowances available in the form of a 30 percent reduction in the taxable income on the total investment for six years, a special withholding tax rate on dividends of 10 percent, and tax losses carried forward for up to 10 years.

|

Examples of Priority Business Sectors and Their Incentives |

|

|

Business line |

Incentive type |

|

Textile and garment industry |

Tax allowance and investment allowance |

|

Pharmaceutical industry |

Tax allowance |

|

Digital economy (hosting, data processing etc.) |

Tax holiday |

|

Geothermal (exploring and drilling) |

Tax allowance |

|

Cooking palm oil industry |

Tax allowance |

|

Iron and steel industry |

Tax allowance |

|

Automotive industry |

Tax allowance |

|

Oil and gas refinery |

Tax holiday |

|

Cosmetics industry |

Tax allowance |

|

Coal gasification |

Tax allowance |

To classify as a priority sector, business enterprises must meet the following criteria:

- Must be labor intensive;

- Must be capital intensive;

- Must be part of a national project/program;

- Must be export-oriented;

- Must involve a pioneer industry (renewables, oil refining, metals, etc.);

- Must utilize advanced technologies; and

- Must implement research and development activities.

Tax allowance for investments in specific sectors and regions in Indonesia

Indonesia’s Government Regulation 78 of 2019 (GR 78/2019), sets out a variety of income tax incentives for businesses investing in specific provinces (such as Aceh, Greater Jakarta, and Riau) and industries, such as marine and fisheries, pharmaceuticals, IT, and energy, among others, in the country.

These incentives come in the form of tax deductions, the accelerated depreciation of fixed tangible assets, and the accelerated amortization of intangible assets. The regulation also increases the period for fiscal loss compensation, in addition to setting the income tax rate on dividends for foreign taxpayers at 10 percent.Deduction in net income of the total investment

The government offers a deduction of the net income by 30 percent of the total investment value. This is charged at five percent per year for six years, in the form of intangible assets, including land.

Accelerated depreciation of tangible fixed assets

The government allows accelerated depreciation of tangible assets, calculated as follows.

|

Type of fixed tangible asset |

Benefit period |

Depreciation rates and method |

|

|

|

|

Straight line method |

Declining balance method |

|

Non-buildings |

|||

|

Category I |

2 years |

50% |

100% |

|

Category II |

4 years |

25% |

50% |

|

Category III |

8 years |

12.5% |

25% |

|

Category IV |

10 years |

10% |

20% |

|

Buildings |

|||

|

Permanent |

10 years |

10% |

– |

|

Non-permanent |

5 years |

20% |

– |

Accelerated amortization of intangible assets

The government allows the accelerated amortization of intangible assets, as calculated below.

|

Type of intangible assets |

Benefit period |

Amortization rate |

|

|

|

|

Straight line method |

Declining balance method |

|

Category I |

2 years |

50% |

100% |

|

Category II |

4 years |

25% |

50% |

|

Category III |

8 years |

12.5% |

25% |

|

Category IV |

10 years |

10% |

20% |

Compensation for losses

There is also compensation available for losses of more than five years but for no more than 10 years.

However, an additional one-year of compensation is granted if investors implement one of several options laid out in the regulation. These are:

- Invest in a sector and region as stated under GR 78/ 2019;

- Invest in industrial or bonded zones;

- Engage in activities related to renewable energy;

- Assign 10 billion Rupiah (US$650,745) on social infrastructure programs;

- Utilize at least 70 percent of domestic raw materials or components by the second year of operations; or

- Employ at least 300 local workers and maintain this number for four consecutive years.

To gain a further two-year extension, investors can:

- Employ 600 Indonesians and maintain this number for four consecutive years;

- Assign at least five percent of their total investment value to research and development aimed at improving their products or services; or

- Export at least 30 percent of their total sales in a fiscal year (applies to specific sectors and are not located in bonded zones).

Reduction in income tax on dividends

Investors can also receive a reduction on their income tax on dividends at a rate of 10 percent. This can be lowered even further if there is an applicable double tax avoidance agreement in place.

Tax incentives for investments in labor-intensive industries, training programs, and R&D

Indonesia’s government provides tax incentives for investments in labor-intensive industries, training programs for local workers, as well as for research and development (R&D) activities.

Labor intensive industries

Taxpayers that invest or expand into labor-intensive or pioneer industries can enjoy a net income reduction of 60 percent of their total investment in the form of tangible fixed assets, which includes any land used for the main business activities over a certain period.

The Ministry of Industry defines a labor-intensive industry as one that employs a minimum of 200 workers with labor costs not exceeding 15 percent of production costs, while the Ministry of Finance defines a pioneer industry as one that provides value-added economic consequences to the surrounding areas, introduces new technologies, and provides strategic value for the national economy.R&D activities

Taxpayers that engage in R&D initiatives can receive a tax facility of 300 percent in gross income reduction of total costs incurred. To avail of this facility, the taxpayer must be conducting R&D that is assessed by the government to be advancing the national economy, new industries, and technologies, or transfer of foreign technology to local businesses.

The maximum 300 percent tax facility covers the following:

- 100 percent reduction on gross revenue for costs of conducting the R&D activities; and

- A maximum 200 percent additional reduction to the gross revenue incurred to conduct the R&D activities within a certain period. This is as follows:

- 50 percent reduction if the R&D generates intellectual property (IP) rights such as in the form of a patent;

- 25 percent reduction if the R&D generates IP rights that are registered domestically as well as abroad;

- 100 percent reduction if the R&D reaches commercialization; and

- 25 percent reduction if the R&D generates IP rights in the form of a patent as defined in (a) and (b), and/or reaches the commercialization stage if the R&D activity is carried out in collaboration with Indonesian R&D institutions or higher learning institutions.

Training programs

Investors looking to start apprenticeship programs or training activities to develop workers based on ‘certain competencies’ can receive a gross income reduction of up to 200 percent of the total costs incurred. The regulation defines certain competencies as developing human resources that can meet the labor requirements needed by national industries and businesses.

Incentives in Indonesia’s special economic zones

Indonesia aims to make its special economic zones (SEZs) a policy priority to attract foreign investment, boost industrial activity, and promote job creation. This strategy has been further facilitated through various incentive programs available throughout the special economic zones in Indonesia.

Exemption on corporate income tax

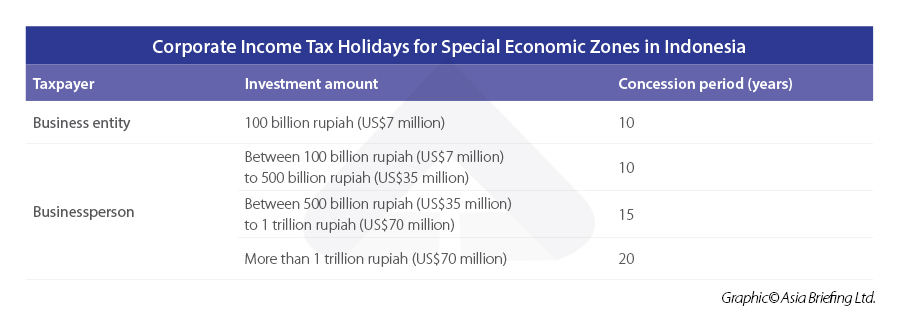

Business stakeholders in an SEZ are differentiated into two types of taxpayers: badan usaha (business entities) and pelaku usaha (businesspersons).

Both business entities and business players are eligible for a 100 percent reduction in corporate income tax (CIT) provided that their investments are conducted in SEZs and with a minimum investment value of 100 billion rupiah (US$7 million), for 10 years.

After the CIT mentioned above incentives expire, taxpayers are eligible for a 50 percent CIT reduction payable for the subsequent two years. Further, during the concession period, no withholding tax (WHT) is applied to eligible income, such as income from land and building rental.

Corporate income tax allowance

Taxpayers that invest 100 billion rupiah (US$7 million) are also eligible to receive several CIT allowances. These are:

- A 30 percent reduction in net income on the total investment on fixed assets reduced over six years over six years, at five percent per year;

- Accelerated depreciation allowances of up to 100 percent of tangible and intangible assets;

- A WHT rate of 10 percent, or the treaty rate (whichever is lower) on dividend payments made to non-resident recipients; and

- Tax loss is carried forward for up to 10 years.

Import and excise duties

Import duties, tax on the importation, and excise duties are all exempted on the following dutiable/taxable goods:

- Capital goods used for the construction or development of SEZs for five years; and

- For the entry of consumable raw materials for service industries (for tourism SEZs); and

- Entry of goods to be sold in shops and shopping centers (for tourism SEZs).

VAT and sales tax on luxury goods

VAT will not be collected in relation to the following activities:

- The import of taxable tangible goods into an SEZ by a business entity;

- The delivery of taxable tangible goods from another Indonesian free trade zone, customs area, or bonded storage facilities to a business entity;

- The delivery of taxable services or goods, including land or buildings by a business entity in an SEZ to another business entity in the same or another SEZ; and

- The import of consumer goods into a tourism SEZ.

The non-collection of VAT also applies to raw materials needed to produce taxable services or goods related to ship and aircraft maintenance, repair, and overhaul (MRO) activities.

Right of foreigners to own apartments and landed houses in special economic zones

Indonesia has made it easier for foreigners to own real estate in special economic zones, free trade zones, industrial zones, or other economic zones (tourism zones, suburban zones, or urban zones).

The properties owned by foreigners are subject to certain restrictions such as:

- Minimum price;

- Land area and number of apartment units;

- Residential zoning; and

- Land space.

The minimum price for landed houses and apartment units varies between provinces.

Immigration

There is special treatment for foreign workers in special economic zones. Foreign workers can obtain temporary resident status for themselves and their families, and they could obtain permanent resident status if they hold property in the SEZ.

Business licenses

The Indonesian government has eased the issuance of business licenses through the Online Single Submission website for investors operating in SEZs.

Right to use, right to build, and right to cultivate for foreign investors

There are several land titles that foreign investors should be aware of. These are:

- Right to manage (Hak Pengelolaan, HPL);

- Right to cultivate (Hak Guna Usaha, HGU);

- Right to use (Hak Pakai, HP);

- Right to build (Hak Guna Bangunan, HGB)

- Right of ownership over stacked units (Hak Milik Atas Satuan Rumah Susun, HMSRS);

- Rights for underground and overground space; and

- Land registration

There are two types of right-to-use (HP) titles:

- Right to use within a certain period; and

- Right to use for land used for specific purposes.

This land title usually refers to the right to use/harvest land directly owned by the state or private land. This land could also be used for a building site in addition to agricultural purposes.

The right to use the title for a certain period can be granted to foreign legal entities that have a representative office, foreign citizens, as well as local entities and citizens. This encompasses state land, freehold title land, and the right to manage land.

If granted for state land and the right to manage land, the title is for a maximum term of 30 years and extendable for another 20. Once the period expires, the title can be extended for another 30 years (a total of 80 years). Previously, an HP title could only be granted for 25 years, and extended for another 20 years, before another renewal of 25 years (a total of 70 years).

The right to build (HGB) is a title that is granted overstate or freehold land to Indonesian citizens and foreign companies (PT PMA) for the purpose of erecting or using a building on the land. The maximum term for an HGB title is 30 years and is extendable for another 20 years. Once this expires, it can be renewed again for another 30 years (80 years in total).The right to cultivate (HGU) is normally granted to state land for the development of plantations and can be granted to foreign companies. The maximum term for this land title is 35 years and is extendable for another 25 years. Upon expiry, this can then be extended by another 35 years.

HGU, HGB, and HP title holders must commence activities on the land, whether building construction, cultivation, or other use of land, within two years of the title being granted.

Incentives for Indonesia’s New Capital City Project

Indonesia’s government offers various fiscal and non-fiscal incentives to businesses seeking to invest in Indonesia’s new capital city, Nusantara.

Nusantara is estimated to cost US$35 billion to construct and the central government is expected to begin operations in the new city in 2024.

Income tax reductions and holidays

The government will provide income tax holidays and reductions for investments in Indonesia’s new capital city. Further, the government will issue future implementing regulations on how the tax facilities will be regulated.

The government will provide up to 100 percent corporate income tax exemption of between 10 and 30 years for domestic taxpayers that invest at least 10 billion rupiah (US$650,745) in the new capital. The duration of the incentive depends on the sectors in which the investment is directed.

For instance, investing in public services will receive the longest tax holiday up until 2035. Banks and insurers that invest before 2035 can enjoy up to 25 years of income tax exemption whereas those that invest before 2045 can receive up to 20 years of income tax exemption.

Developers of other critical infrastructure, such as public works, airports, seaports, and housing, can also benefit from the incentives, as well as businesses that engage in economic development through the construction of hotels, malls, energy infrastructure, and software, among many others.

Corporate income tax reductions will be available for investors that develop financial centers in the new capital, as well as for companies that relocate their head offices to the new capital. Moreover, investors that implement certain research and development activities will be afforded a reduction in their gross income.

Further, micro, small, and medium-sized enterprises in certain business activities will also pay a zero percent corporate income tax rate.

Utilization of foreign workers

Businesses operating in the new capital city will be allowed to employ foreign workers for 10 years; this can also be extended. The foreign worker can also secure residency permits for 10 years, which is also extendable depending on their employment contract.

The employer is also exempted from paying the Foreign Worker Compensation Fund, which is the amount of US$100 paid every month to the Ministry of Manpower.

The residency permits of foreign workers who hold management positions in companies operating in the new capital will remain valid as long as they retain that said position.

Land rights

The government is offering investors 95-year land use permits, which can be extended for another 95 years and thus totaling 190 years for land use.

There will be two categories of land in Indonesia’s new capital: a) state-owned property that will be managed by the Nusantara Capital City Authority (a special agency tasked with governing and managing the new capital city) and b) assets that have been granted to the capital city authority through the right-to-manage (Hak Pengelolaan – HPL) deed titles.

The capital city authority can allocate these HPL lands to businesses for the following land rights/titles:

- Right to cultivate (Hak Guna Usaha – HGU);

- Right to build (Hak Guna Bangunan – HGB); and

- Right to use (Hak Pakai – HP).

The right to cultivate title (HGU) gives the user the right to work/cultivate the land for a specific period. This type of land title is usually granted for agricultural activities, such as plantations. In Indonesia’s new capital, holders of the HGU title will be allowed to cultivate the land for 95 years, which can then be extended for another 95 years, totaling 190 years.

This is a huge increase compared to other parts of Indonesia where the HGU title is valid for 35 years and extendable for another 35 years upon expiration.

The right to build title (HGB) is granted to Indonesian citizens and foreign companies to erect a building on the land. HGB title holders will be eligible to hold the title for 80 years, which can be extended for another 80 years, totaling 160 years.

Outside of Nusantara, HGB title holders can only hold the title for 30 years, and extendable for 20 years. Once this period has expired, the title can be renewed for another 30 years, so 80 years in total.Finally, right-to-use (HP) title holders will also be given 80 years and extendable for another 80 years. This title refers to the right to use or harvest the land owned by the state or private persons.

Outside of the new capital city, the HP title is granted for 25 years and extended for another 20 years, before a final renewal of 25 years, totaling 70 years.

Customs

The government offers exemptions on import duties for the import of goods used for the construction and development of Indonesia’s new capital. Further, there are import duty exemptions for the import of goods and materials used in the construction and development of industries within the new capital.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City, and Da Nang in Vietnam, in addition to Jakarta, in Indonesia. We also have partner firms in Malaysia, the Philippines, and Thailand as well as our practices in China and India. Please contact us at asean@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Incentivi per il progetto della nuova capitale dell’Indonesia

- Next Article Singapore and EU Sign Digital Trade Agreement