Tax Incentives for Special Economic Zones in Indonesia

The Indonesian government has pledged to make the special economic zones (SEZs) a policy priority to attract foreign investment, boost industrial activity, and promote job creation. This strategy has been further facilitated through various tax incentive programs by Indonesia’s Ministry of Finance.

These tax incentives include exemptions from income tax, value-added tax (VAT), import duties, sales tax on luxury goods, and excise duties.

As of 2022, there are 19 SEZs in Indonesia of which 12 are in operation and the remainder are in the construction phase. Eight are designated for tourism with the rest for manufacturing and processing.

In establishing the SEZs, the government has sought to diversify away from the island of Java and spread across the country. As of 2021, Indonesia’s SEZs have attracted just over US$5 billion in investments, and employ over 28,000 workers. The island of Java contributes some 60 percent of the total Indonesian GDP and accounts for 60 percent of the country’s total population of 270 million.

What tax incentives are available?

Proposing an SEZ

Indonesian businesses or regional governments can propose an area for the development of an SEZ if they adhere to the following criteria:

- The proposed land is not a protected area, nor does it have the potential to disturb protected areas. The land must also be in accordance with regional spatial plans;

- At least 50 percent of the required proportion of the land must already be possessed; and

- The land must have clear boundaries.

Exemption on corporate income tax

Business stakeholders in an SEZ are differentiated into two types of taxpayers: badan usaha (business entities) and pelaku usaha (businesspersons).

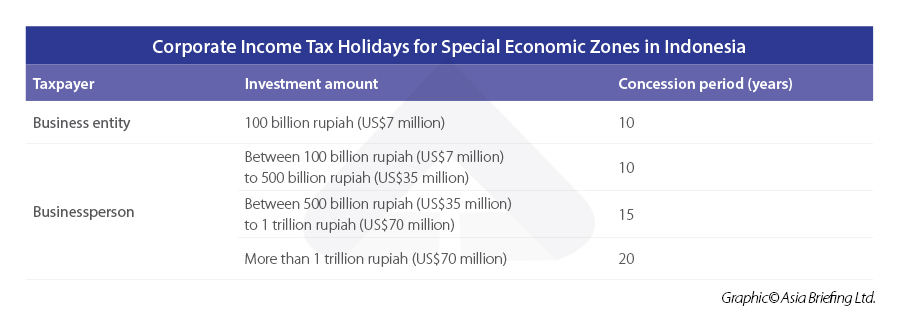

Both business entities and business players are eligible for a 100 percent reduction in corporate income tax (CIT) provided that their investments are conducted in SEZs and with a minimum investment value of 100 billion rupiah (US$7 million), for a period of 10 years.Businesspersons can receive more concession period – the greater their investment – as seen from the following table.

After the CIT mentioned above incentives expire, taxpayers are eligible for a 50 percent CIT reduction payable for the subsequent two years. Further, during the concession period, no withholding tax (WHT) is applied to eligible income, such as income from land and building rental.

Corporate income tax allowance

Taxpayers that invest 100 billion rupiah (US$7 million) are also eligible to receive several CIT allowances. These are:

- A 30 percent reduction in net income on the total investment on fixed assets reduced over six years over six years, at five percent per year;

- Accelerated depreciation allowances of up to 100 percent of tangible and intangible assets;

- A WHT rate of 10 percent, or the treaty rate (whichever is lower) on dividend payments made to non-resident recipients; and

- Tax loss is carried forward for up to 10 years.

Import and excise duties

Import duties, tax on the importation, and excise duties are all exempted on the following dutiable/taxable goods:

- Capital goods used for the construction or development of SEZs for a period of five years; and

- For the entry of consumable raw materials for service industries (for tourism SEZs); and

- Entry of goods to be sold in shops and shopping centers (for tourism SEZs).

VAT and sales tax on luxury goods

VAT will not be collected in relation to the following activities:

- The import of taxable tangible goods into an SEZ by a business entity;

- The delivery of taxable tangible goods from another Indonesian free trade zone, customs area, or bonded storage facilities to a business entity;

- The delivery of taxable services or goods, including land or buildings by a business entity in an SEZ to another business entity in the same or another SEZ; and

- The import of consumer goods into a tourism SEZ.

The non-collection of VAT also applies to raw materials needed to produce taxable services or goods related to ship and aircraft maintenance, repair, and overhaul (MRO) activities.

Eligibility criteria

To be eligible for all the mentioned incentives, businesses will need to meet the following conditions:

- Business license;

- Evidence of being a domestic corporate taxpayer;

- Have approval from the Indonesian Investment Coordinating Board, based on the company’s standard industrial classification (KBLI);

- Location of the project; and

- Determination of the type of production/services to be conducted.

Webinar – Diversify Your Business to Indonesia – The Ins and Outs of Set Up

5:00 PM China Time / 4:00 PM Vietnam / 10:00 AM CET

Oct. 20, 2022 | 10:00 AM Los Angeles / 1:00 PM New York Discover why, where, and how to set up in Indonesia, as well as what type of investment is permitted along with taxes and other costs involved with operating a business in Indonesia.

Join us in this free webinar!

Also, Read

- Opportunities in Indonesia’s Special Economic Zones – Latest Issue of ASEAN Briefing Magazine

- Indonesia Considers an SEZ on Natuna: Investment Prospects, Challenges

- Comparing Mexico and Indonesia as Manufacturing Hubs for US Investors

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City, and Da Nang in Vietnam, Munich, and Essen in Germany, Boston, and Salt Lake City in the United States, Milan, Conegliano, and Udine in Italy, in addition to Jakarta, and Batam in Indonesia. We also have partner firms in Malaysia, Bangladesh, the Philippines, and Thailand as well as our practices in China and India. Please contact us at asia@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Establishing a Representative Office in Thailand

- Next Article 2023 Foreign Investment Opportunities in Singapore