Indonesia’s Income Tax Incentives: Opportunities in Specific Sectors and Regions

- The Indonesian government introduced Regulation 78 of 2019, offering a variety of income tax incentives for investments in specific industries and provinces.

- These incentives include tax deductions, the accelerated depreciation of fixed tangible assets, and the accelerated amortization of intangible assets, among others.

- The development bodes well for businesses as the tax allowance schemes have been expanded to 183 from 145 sectors.

Indonesia’s government on December 13, 2019, issued Government Regulation 78 of 2019 (GR 78, 2019), which sets out a variety of income tax incentives for businesses investing in specific industries and provinces in the country.

These incentives come in the form of tax deductions, the accelerated depreciation of fixed tangible assets, and the accelerated amortization of intangible assets. The regulation also increases the period for fiscal loss compensation, in addition to setting the income tax rate on dividends for foreign taxpayers at 10 percent.

GR 78, 2019, along with GR 45, 2019 (which was issued earlier this year) are designed to encourage more foreign investment and develop major industries. As such, investors should seek the assistance of registered local tax advisors to better understand how these incentives can best benefit their business.

What are the criteria for the incentives?

Investors will need to meet various requirements to be eligible for the incentives under GR 78, 2019.

They are only allowed to:

- Invest in specific sectors as listed in Appendix I of the regulation (page 28); and

- Invest in specific sectors in certain provinces in Indonesia as listed in Appendix II of the regulation (page 71).

These sectors include pharmaceuticals, geothermal energy, and IT, among others

Additionally, investors must:

- Prove that their investments are of high-financial value;

- Prove that the sector they are investing in is export-oriented;

- Have their business absorb a large workforce (labor-intensive); and

- Utilize high volumes of local content in any production process.

Net income deduction

Taxpayers that fulfil the aforementioned requirements are eligible to receive a net income reduction of 30 percent of their total investment of any fixed tangible assets. This incentive is granted for up to six years with annual deductions set at five percent.

The fixed tangible assets (which includes land) must be utilized in core business activities. The assets must also be documented on principal business and investment permits, as well as investment registration certificates. Moreover, the assets must be obtained in new condition, unless it is being imported or relocated from overseas.

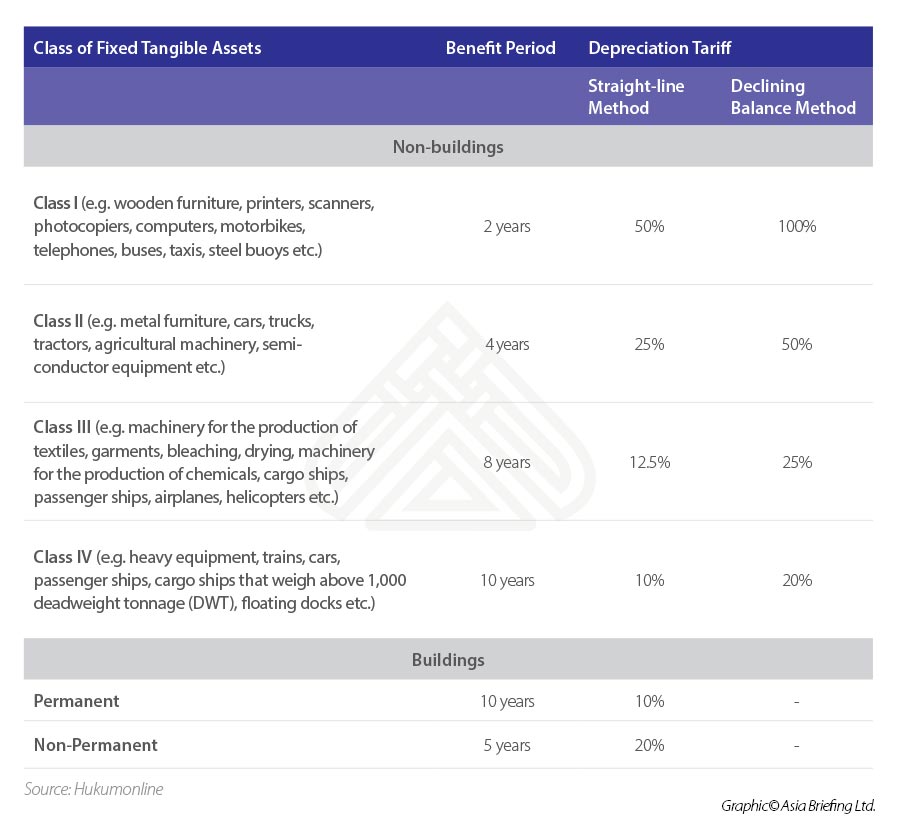

Accelerated depreciation of assets

Under GR 78, 2019, taxpayers are eligible to receive a tax incentive in the form of the accelerated depreciation of their fixed tangible assets. This type of depreciation reduces the taxable income much earlier in the life of the asset and thus businesses can reduce their tax liability.

There are two methods to measure depreciation used in the regulation: straight-line method, and the declining balance method.

Under the straight-line method, the depreciating value of the asset is spread evenly for every year the asset is still functional, useful, and profitable. The formula for calculating straight-line depreciation is as follows:

Straight-line depreciation = (cost of the asset- estimated salvage value (value of an asset at the end of its residual life)) ÷ estimated useful life of the asset.

Through the declining balance method, a constant percentage decrease is applied to the value of the asset each year. This results in greater depreciation in the early years of the asset and smaller depreciation in the later years.

GR78, 2019 sets out the two methods and their new depreciation percentages as well as the length of the benefit periods below:

Accelerated amortization of intangible assets

GR 78, 2019 allows taxpayers to accelerate the amortization of their intangible assets. The benefit period and depreciation tariffs are as follows:

Fiscal loss compensation

In Indonesia, businesses that are operating at a loss can be compensated in the following tax period for up to five years. Under GR 78, 2019, this period can be extended for up to 10 years.

An additional one-year of compensation is granted if investors implement one of several options laid out in the regulation. These are:

- Invest in a sector and region as stated under GR 78, 2019;

- Invest in industrial or bonded zones;

- Engage in activities related to renewable energy;

- Assign 10 billion Rupiah (US$714 thousand) on social infrastructure programs;

- Utilize at least 70 percent domestic raw materials or components by the second year of operations; or

- Employ at least 300 local workers and maintain this number for four consecutive years.

To gain a further two-year extension, investors can:

- Employ 600 Indonesians and maintain this number for four consecutive years;

- Assign at least five percent of their total investment value to research and development aimed at improving their products or services; or

- Export at least 30 percent of their total sales in a fiscal year (applies to specific sectors and are not located in bonded zones).

Imposition of dividends

The new regulation states that the rate of income tax on dividends paid to foreign taxpayers who do not have a permanent establishment in Indonesia is set at 10 percent; unless there is an applicable double tax agreement (DTA) in place, from which the lower rate between the two countries is used.

OSS submission

To apply for these incentives, taxpayers will need to submit their application to the government’s Online Submission System (OSS), and the approval will be issued within five working days.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City and Jakarta. Please contact us at asia@dezshira.com or visit our website at www.dezshira.com.