Key Industries for Investment in ASEAN

By Matthew Zito, Benedict Lynn, and Emily Liu

As ASEAN continues its transition to greater economic integration with the implementation of the ASEAN Economic Community in 2015, the region is seeing strong growth in a number of industries. Among the key business areas are electronics, information and communications technology, textiles and apparel, and medical devices. Foreign investors seeking to find the next manufacturing destination after China, would be well advised to look closely at this dynamic region. In this article we provide a snapshot into each industry and provide context within the wider ASEAN region.

Electronics

The electronics sector has long been a major force in ASEAN’s rapid economic development, and continues to rise. In 2010, total ASEAN electronics exports accounted for over US$195 billion, or 18 percent of the region’s total exports, and last year electrical and electronic (E&E) product exports from East Asia Pacific (EAP) countries (31 percent of total exports in developing EAP nations) grew 9.2 percent, up from 7.8 percent in 2012 and 8.7 percent in 2011.

Traditionally it was China, with its vast and cheap labor force, where parts supplied by ASEAN-4 countries (Indonesia, Thailand, Malaysia, Philippines) and financed by the EAP’s high-income countries, such as Japan and New Zealand, would be assembled and shipped to the rest of the world. However, China’s recent rise up the export market value chain from mass manufacturing to more high-tech products, as well as its rising labor costs, have resulted in a shift of FDI to ASEAN’s Mekong countries (Myanmar, Thailand, Cambodia, Vietnam).

In particular, Vietnam has emerged as an important electronics exporter, with E&E products overtaking coffee, textiles and rice to become the country’s top export item in 2012, as well as capturing a six percent share of the computer and telecom equipment market, up from zero. The country has recently attracted substantial investments from multinational giants such as Samsung and Mitsubishi, and analysts predict that once Thailand moves up the value chain, Vietnam will take its place.

Thailand, long a global leader in the manufacture and export of computer hard-disk drives, saw its electronics-related FDI more than triple in 2010. However, the global shift away from PCs to tablets resulted in its hard-disk drive exports contracting by 5.6 percent last year. Despite this, due to the countries continued strong exports in other E&E products such as radios, TVs and printers, a recent Credit Suisse report not only rated Thailand as the region’s most competitive country in electronic exports over the last 15 years, but also forecasted it to rank top among ASEAN countries in 2013.

Singapore’s well-established electronics industry generated a manufacturing output of S$86.1 billion (US$ 68.86 billion) in 2011. As ASEAN’s de facto commercial center, its highly educated workforce, reliable business environment and transparent legal and tax regimes have ensured that Singapore remains a popular destination for global electronics companies, with electronics accounting for 45 percent of all investments in 2010.

From 2011 – 2013, however, the city state’s reliance on PC and semiconductor manufacturing as well as its rising labor and energy costs have resulted in a year-on-year contraction in its electronics cluster. Singapore will have to adapt to the needs of the global market – shifting its focus to higher growth industries – and manage costs if they are to compete with emerging economies such as Thailand and Vietnam. But this should not pose a problem to highly developed and wealthy Singapore, nor will the large manufacturers be relocating any time soon.

Information and Communications Technology (ICT)

Historically, the information and communications technology (ICT) sectors have remained some of the most closed to foreign investment in ASEAN. Between 2010 – 2013, in direct response to the imposition of foreign owned restrictions (FORs) in telecommunications, FDI to Indonesia’s tertiary sector dropped by over 30 percent (US$3 billion), while in the Philippines, foreign equity in the same area is constitutionally limited to 40 percent.

However, as ASEAN marches ever closer to total economic integration in 2015, great strides are being taken to both further regional cooperation between the group, with members at varying degrees of ICT development, and to open up the sector to the rest of the world.

One such initiative is the ASEAN ICT Masterplan 2015 (AIM2015), which seeks to expand the reach of services, such as broadband and telecommunications infrastructure, further develop innovation capacity, and encourage FDI. Since its launch in 2011, as many as 60 related projects have been undertaken, ranging from capacity building and training workshops to the development of regional frameworks for cooperation and coordination in areas such as electronic government, cyber security and policy and regulations.

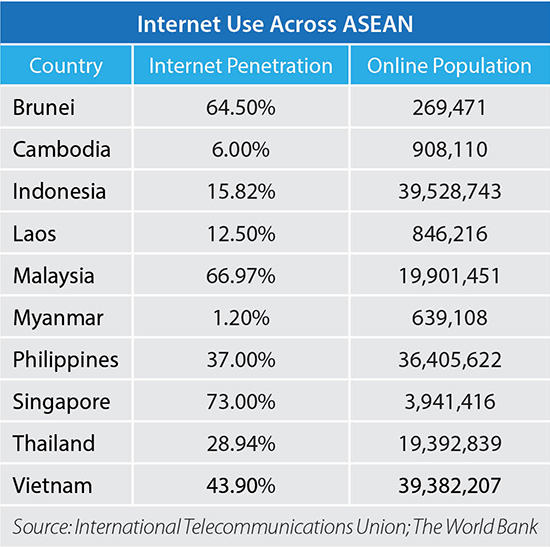

The industry has been developing at a remarkable pace and currently employs over 11.7 million people across the region, contributing more than US$32 billion, or over three percent, of ASEAN’s GDP. Mobile penetration and internet penetration across all member states, which make up the second largest community of Facebook users in the world, stand at 110 and 25 percent, respectively. Vietnam, Indonesia, and the Philippines each have a subscriber base of over 100 million.

The region’s large, young, tech-savvy population is shifting from feature phones to smart phones, which currently make up about 66 percent (and rising) of ASEAN’s mobile market. Despite this, the market (largely dominated by Android devices) remains far from saturation, with mobile commerce opportunities continuing to increase.

A recent Mastercard study rates hyperconnected Singapore (which has the fourth highest smartphone penetration in the world and 73 percent of its population online) as the most mobile payment ready member state, followed by the Philippines, Malaysia and Thailand. At the other end of the scale is Myanmar, which only has one percent of its population online along with underdeveloped telecoms networks, infrastructure and power grids. However the newly outward-looking republic has been making significant efforts toward open up its telecommunications sector, and hopes to achieve 50 percent wireless accessibility by 2015. In January of this year, in an unprecedented move, formal licenses to operate networks in Myanmar were granted to two foreign telecoms giants, Telenor and Ooredoo. A target has been set to raise the country’s mobile penetration rate from nine percent to 80 percent by 2016.

Indonesia, also known for its restrictive ICT sector, already has 282 million mobile subscriptions and is expected to have 100 million Internet users by 2016. Jakarta, (alongside Bangkok) has the highest density of Facebook users in the world and the Nusantara Super Highway (currently under construction) will expand broadband penetration to even the country’s most rural provinces.

Whether in Malaysia, seeking to privatize its telecoms industry, Thailand and Indonesia, with their rapidly growing middle class and broadband initiatives, or even developing Myanmar, with its projects for improving infrastructure, opportunities abound across ASEAN’s ICT sector. In 2010 exports in information-technology products accounted for more than a quarter of the region’s total exports, at US$ 258 billion. As FORs and other barriers to foreign equity continue to be relaxed or wholesale abolished, investment is only likely to rise in this very exciting growth industry.

Textiles and Apparel

Another industry to watch for foreign investment opportunities in the lead up to AEC 2015 is textiles and apparel. Long a bulwark of China’s manufacturing sector, textiles and apparel represents a fast-rising sector in the greater ASEAN economy, where it is the largest industrial employer in the majority of member states. Early on, the importance of textiles to the ASEAN economy was marked by its inclusion as one of 11 sectors selected for accelerated regional integration as part of the Vientiane Action Programme (2004).

It is not simply the case, however, that ASEAN stands to siphon off production from China; rather, in addition to the region’s rise as a low-cost manufacturing center, ASEAN is also the fastest growing export market for Chinese textiles (30 percent year-on-year in 2013), and China’s third largest export market overall, as facilitated by the China-ASEAN Free Trade Area agreement. Additionally, in a recent report by Standard Chartered, apparel and clothing was identified as one of six areas in which Indian exports to ASEAN could boom in the coming years.

Within ASEAN, Vietnam is the strongest competitor for inheriting low value-added textiles and apparel manufacturing from China. In contrast to other leading textile exporters in the region (Indonesia, Thailand, Malaysia), the share of Vietnam’s textile exports against its total exports has grown in recent years, based on WTO figures. As of 2012, there were over 3800 companies in the industry in Vietnam, the majority of which are cut-and-sew enterprises. The industry’s comparative lack of upstream suppliers, where various fabrics and accessories must be imported from outside Vietnam, makes it a prime candidate for regional integration.

Textiles consistently ranks among Vietnam’s leading export industries, employing upwards of 1.3 million workers in directly related jobs and more than 2 million with auxiliary work included. The country’s voracious demand for cotton (400,000 megatonnes consumed in 2012) is primarily fed by the U.S., India and South Africa.

Vietnamese-produced yarn is then exported to buyers in China, Korea and Turkey. Vietnam has set targets for 2020 of increasing investment capital in its textiles industry to US$25 billion and the related workforce to 3 million.

Cambodia’s textile and apparel industry faces similar problems as that of Vietnam in terms of moving up the value-added chain, albeit on a smaller scale. Nevertheless, the country’s production capacity exceeds 500 factories staffed by upwards of 500,000 textile and apparel workers. Low wages and weak enforcement of labor laws, however, have led to endemic volatility in the industry and hesitation on the part of foreign investors to continue sourcing from the country.

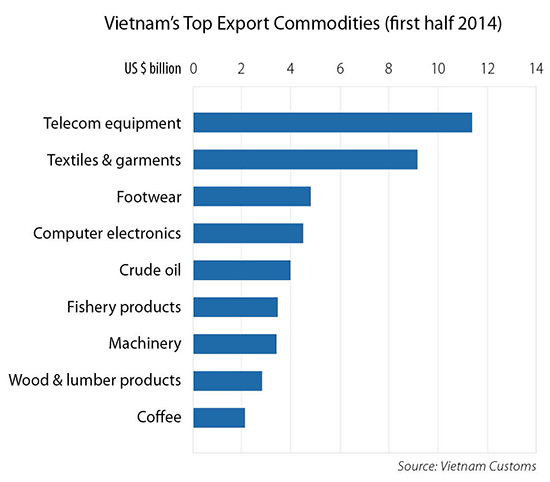

Overall, challenges remain for creating an intra-ASEAN comprehensive supply chain for the textiles industry capable of competing on a global footing. Such is the aim of the Source ASEAN Full Service Alliance (SAFSA) established in 2010 by the ASEAN Federation of Textile Industries (AFTEX). Within the region, the Thai and Vietnamese apparel industries are already very closely tied: bilateral trade in garments reached US$160 million in the first half of 2014, which was heavily weighted toward imports into Vietnam.

Medical Devices

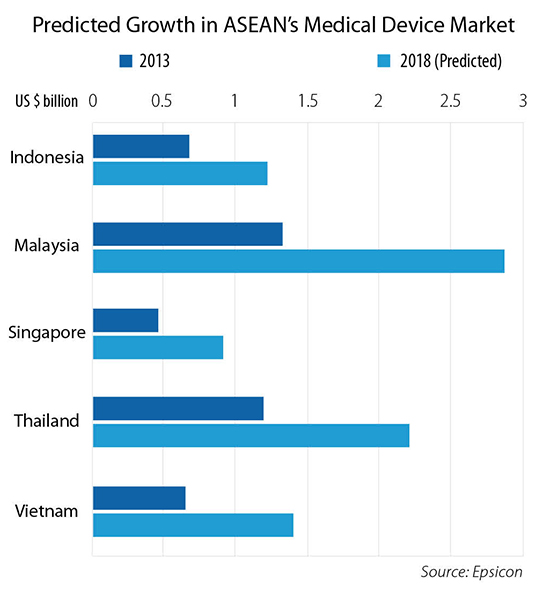

A rapidly expanding middle class and, for some, the beginnings of a greying population, has been driving the boom in trade of medical devices in the region. ASEAN’s medical device market, which was worth about US$4.6 billion in 2013, is expected to double to US$9 billion by 2019, according to Pacific Bridge Medical.

Local medical device markets within the region have been charting double digit growth rates in recent years, and will likely continue to do so. With the increased demand for better healthcare, encouraged by governmental focus on healthcare as a priority sector for trade and service liberalization under the AEC Blueprint, the upside market potential for medical devices in the region is immense.

Currently, the individual medical device markets across ASEAN’s ten member countries are in various stages of development. Countries such as Malaysia and Indonesia, which are rich in rubber, lead global production in latex products such as surgical gloves and syringes. Singapore, the region’s medical and technological hub, has a thriving biomedical research and development industry, and a strong comparative advantage in the advanced manufacturing skills valued for medical manufacturing, including precision engineering.

In recent years, Thailand has been gunning to become the next regional medical hub, with its Healthcare 2020 Masterplan. Together, Malaysia, Indonesia, and Thailand make up about 65 percent of the current medical device market in ASEAN.

On the regulatory side, countries have made significant strides towards developing a mature regulatory framework for medical devices, both individually and regionally. In 2012, Malaysia introduced its first set of medical device regulations under its Medical Devices Act 2012, making it mandatory for all medical devices to be registered with the Medical Devices Authority (MDA). Brunei, Cambodia and Laos are still in the midst of developing their own requirements.

After years of negotiations, the ASEAN Consultative Committee on Standards and Quality’s Medical Device Product Working Group (ACCSQ – MDPWG) has finalized the ASEAN Medical Device Directive (AMDD), a set of non-legally binding stipulations to harmonize regulations across the region, in line with its aim to liberalize trade and investment in the healthcare sector under the AEC Blueprint. The AMDD is expected to take effect on January 1, 2015, and will mark a significant step towards promoting easier access for medical device companies to the regional market of more than 600 million people.

At present, ASEAN countries are still reliant on imports to feed their demand for medical devices. As much as 97 percent of the medical devices consumed in Indonesia in 2013 were imported, mainly from the United States, Japan and Europe. Nevertheless, momentum is building for local manufacturing to transition towards higher- level products, as foreign companies move into the region to take advantage of the lower costs and rising demand.

In Malaysia, which produces about 62 percent of the world’s rubber gloves and 79 percent of its catheters, diagnostic imaging exports have been growing in recent years, particularly in electrocardiographs and other electrodiagnostic apparatus, according to research by Espicom. In December, operations at Malaysia’s first diagnostic imaging systems manufacturing base by Toshiba Medical Systems are slated to begin. Espicom estimates the country is likely to see compound annual growth of 16.1 percent to 2018, with growth for consumables as high as 24.8 percent.

Singapore, a leading regional and global biomedical hub, is home to more than 30 medical technology firms that have set up manufacturing bases in the island-nation, according to its Economic Development Board. All of the largest medical technology firms also have their regional headquarters in Singapore, tapping the state’s extensive entrepôt trading network.

Throughout the region, strong governmental support is accelerating growth for the industry. In Thailand, the Board of Investment offers incentives for investors interested in manufacturing medical equipment in the country, ranging from import duty exemptions for machinery, to tax breaks and land ownership rights for foreign investors. In April 2012, the Thai government announced approval of a plan to establish a medical industrial park for manufacturers of medical devices in the country, hoping to raise Thailand’s medical device exports to 30 percent of the global market in the near future.

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email asean@dezshira.com or visit www.dezshira.com.

Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight.

Related Reading

Tax, Accounting, and Audit in Vietnam 2014-2015

Tax, Accounting, and Audit in Vietnam 2014-2015

The first edition of Tax, Accounting, and Audit in Vietnam, published in 2014, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in Vietnam, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in Vietnam in order to effectively manage and strategically plan their Vietnam operations.

An Introduction to Tax Treaties Throughout Asia

An Introduction to Tax Treaties Throughout Asia

In this issue of Asia Briefing Magazine, we take a look at the various types of trade and tax treaties that exist between Asian nations. These include bilateral investment treaties, double tax treaties and free trade agreements – all of which directly affect businesses operating in Asia.

- Previous Article Asia Heavyweights Show Interest in Singapore-Malaysia High Speed Rail Link

- Next Article Singapore to Reduce Property Taxes for HDB Flats