Investment Hotspots in the Philippines: Promising Sectors to Watch

The Philippines was among the world’s fastest-growing emerging markets in 2022, recording a GDP of 7.6 percent. This also represented the country’s fastest growth since 1976.

The Southeast Asian nation is working to reduce its reliance on overseas remittances and has gradually developed its domestic industries to move up global value chains in select industries, thereby presenting foreign investors with newfound opportunities. Some of the most dynamic sectors in the Philippines are business process outsourcing and semiconductor manufacturing, which are slowly contributing to a larger portion of the GDP.

Business process outsourcing

The BPO industry in the Philippines is important for the country’s economy and contributed around US$32.5 billion in 2022, an increase of 10 percent from 2021. The industry has improved its capacity to offer non-call center outsourcing solutions and is ripe for investments into more value-added levels of outsourcing, namely knowledge process outsourcing (KPO). This comprises of IT outsourcing, animation game development, financial research, software development, and data analytics, among others.

The economic contribution of the Philippines’ BPO industry is expected to outpace further remittances sent from Filipinos working abroad. Remittances were an important stabilizing factor for the country’s economy during the height of the pandemic in 2020 and 2021, contributing to some 10 percent of GDP, making the Philippines the country with the highest remittances to GDP ratio in Southeast Asia. Remittances to the Philippines hit a record high of US$36 billion in 2022.

However, it is expected that the ratio of remittances will begin to decrease as revenue from local industries such as BPO begins to fill the gap. For instance, revenue from BPO activities now contributes to approximately 11 percent of GDP.

The Philippines now controls between 10-15 percent of the global BPO market, employing over 1.3 million Filipinos in over 1,000 BPO companies, including Accenture, Wipro, and Simens. The industry has thrived since the 1990s – the workforce’s proficiency in speaking American-accented conversational English is instrumental to the industry’s success. Further, tax incentives and low operating costs are frequently cited as reasons why the BPO industry has boomed in the Philippines, to a point where the country is recognized as the ‘call center capital of the world’.Industry experts expect annual BPO revenues to reach US$59 billion by 2028, at an annual growth rate of approximately 10.4 percent.

The KPO industry

The KPO sub-sector in the Philippines has become a significant contributor to the development of the country’s BPO industry. Further, as special economic zones (SEZs) permitted the work-from-home setup for BPO companies, they have been able to expand their scope of services to clients – opening the door for investments into high-value KPO sub-sectors like game animation, IT services, banking, and financial services, legal services, and data analytics, among many others. Higher-value KPO services will increasingly become more attractive investments as the outsourcing industry braces for the automation of voice-based services.

As such, the KPO industry allows companies to find and work with highly trained professionals combined with top-tier technology to help businesses grow. Importantly, KPO services help businesses become more flexible by allowing them to scale up or down depending on industry demands.

Skills upgrade programs are also being implemented across BPO sectors amid the threat of robotic process automation and artificial intelligence (AI). Further, BPO companies could also utilize AI tools to deliver more value for their clients.

Electronics and semiconductors

The Philippines’ electronics sector is one of the biggest contributors and the backbone of the country’s manufacturing output.

The export of electronics and semiconductors are expected to reach US$50 billion in exports for 2023, rising from US$45.92 billion in 2022. The electronics industry is classified into 73 percent semiconductor manufacturing services and 27 percent electronics manufacturing. The export of semiconductors makes up 47 percent of the total goods exported from the Philippines, or the equivalent of US$29.2 billion.

Through greater foreign investments, the Philippines is also aiming to attract investments that will move up the global value chain. There is a need to upgrade the industry’s global value chain participation, especially in areas with high growth potential such as consumer electronics, power electronics, biomedical electronics, and auto electronics. Some of the leading companies in this industry include Fastech Synergy Philippines Inc, Amkor Technology, and Megachip Semicon Electronics Corp.

Further, through the passing of the CHIPS Act in the United States, the Philippines can become a hub for semiconductor assembly and test manufacturing. Although the CHIPS Act incentivizes microchip manufacturers to produce in the US, there are aspects of the semiconductor supply chain such as assembly, testing, and packaging which can be done more cost-effectively outside the US.

In addition, the Philippines has an established pool of skilled talent in the areas of information technology and engineering. Coupled with a low-cost labor force and government incentives, the country is an attractive destination for investors seeking to expand their semiconductor operations.

The Semiconductor and Electronics Industries in the Philippines Foundation, Inc. (SEIPI), the largest organization of foreign and Filipino electronic businesses in the country, expects the electronics industry to reach a six percent annual export growth and hit US$50 billion in exports by 2030.

Agriculture

The value of the top 10 agricultural exports in the Philippines was valued at US$6.49 billion in 2022, or 95 percent of the total agricultural export revenue. The country’s main agricultural products include rice, coconuts, sugarcane, corn, bananas, pineapples, and mangos.

The sector also contributes to an estimated 8.9 percent of GDP in 2022 and employs 24 percent of the local workforce. However, agriculture has only grown around two percent per year in real terms, compared with the economy’s five percent growth. Further, the sector is plagued with low levels of mechanization and the country has one of the region’s oldest farmers with an average of 57.

The Philippines, being one of the most disaster-prone countries in the world due to its location in the Pacific Ring of Fire and subject to typhoons every year, has gradually shifted to high-value and high-yielding crops to boost production totals. The country is encouraging investments in areas like AgriTech to not only drive-up yields but also improve irrigation and infrastructure to reduce export-related costs and food wastage.A three-year agriculture development program is currently in the works with the aim to promote agricultural productivity, particularly in rice, corn, high-value crops, poultry, fisheries, and livestock. Moreover, the Philippines aims to achieve rice self-sufficiency by 2025 with areas not competitive in rice production to be converted to crops such as bananas and coconuts.

In line with this program, investors can also offer their expertise in logistics improvement, research and development, and postharvest and processing.

The digital economy

The Philippines’ digital economy had a gross merchandise value (GMV) of US$20 billion in 2022, at a compound annual growth rate (CAGR) of 22 percent. The GMV is expected to rise to US$35 billion in 2025 and between US$100 billion to US$150 billion by 2030.

There are significant opportunities for foreign investors in the Philippines’ e-commerce sector, which has been the main growth driver of the country’s digital economy. Lazada and Shopee recorded over 100 million visits combined in 2022.

The industry recorded a GMV of US$14 billion in 2022 and this is predicted to increase to US$22 billion in 2025. As such, digital technologies have the potential to unlock significant economic value in the Philippines especially since between 68 to 72 percent of the population has access to the internet and some 86 million use smartphones, or roughly 77 percent of the population.

Foreign investors can also provide solutions in cloud computing, financial technology (FinTech), the Internet of Things, and big data for various Filipino industries. Importantly, FinTech can help improve financial inclusivity in the country, serving the underbanked and unbanked population.

The country’s central bank estimates that 56 percent of the population has a bank account; however, some 30 million are still unbanked. FinTech firms can make financial services more affordable and accessible for the unbanked and underbanked population. The Philippines has a growing startup ecosystem with a strong focus on digital payments, lending, and remittances, which are all areas of high demand in the country.

Moreover, many micro, small, and medium-sized businesses have little access to formal financing from banks because many are operating in the informal sector, and as a result, they do not pass the stringent requirements from banks. FinTech firms can plug this gap for financing by providing microloans which can be disbursed within 24 hours and the terms and maturity are small and short – usually less than US$100.

Renewable energy

The Philippines has an estimated 246,000 megawatts (MW) of untapped renewable energy. It has the world’s third-largest geothermal capacity at 1,900 MW with Indonesia in second and the US on top.

The country’s current mix of renewable energy consists of 4.3 gigawatts (GW) of hydropower, 896 MW from solar energy, and wind 427 MW. The Philippines adopted an ambitious plan to increase the share of renewable energy in the power generation mix to 35 percent by 2030 and 50 percent by 2040.

This involves increasing geothermal capacity by 75 percent, expanding hydropower capacity by 160 percent, increasing wind power capacity to 2,345 MW, and adding an additional 277 MW of biomass power. The Department of Energy estimates the country needs US$120 billion by 2040, presenting ample opportunities for foreign investors.

Webinar – Future-Proof Your Business: De-Risking Your Supply Chain in Asia

August 23, 2023 | 9:00 AM PDT / 12:00 PM EDT

In this webinar, a panel of Business Intelligence Leaders will help you understand key differences between the main markets in South / Southeast Asia and discuss their evolving supply chain ecosystems, enabling you to make informed decisions to de-risk your supply chain.

Infrastructure

The Philippines has for decades struggled with inadequate infrastructure to serve its 113 million people, resulting in the country having the highest logistic costs in ASEAN. Traffic in Manila alone costs the economy US$17.5 billion annually.

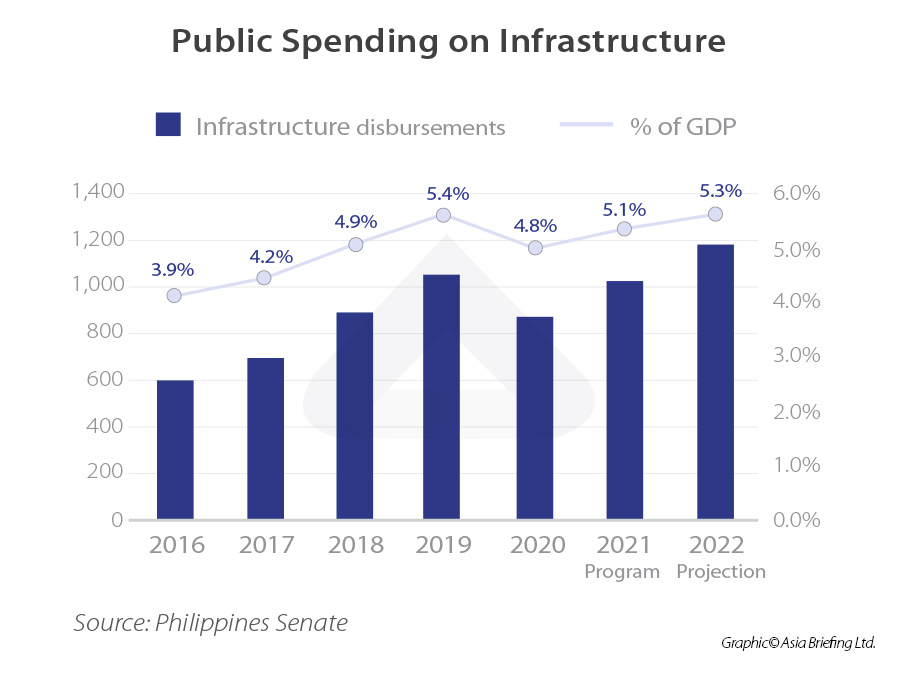

Previous President Duterte promised to usher in the country’s ‘golden age of infrastructure’ with his centerpiece US$162 billion ‘Build, Build, Build (BBB) program. Through the program, his administration was able to increase infrastructure spending from only 3.9 percent of GDP when his term started in 2016 to 5.3 percent at the end of his tenure in 2022.Moreover, under the program, more than 40,000km of roads were built, rebuilt, broadened, and preserved, including 3,101km of tourism roads, while 6,854 bridges were built. Some 11 airports were built, expanded, or upgraded, and three new seaports were built.

There are key opportunities for foreign infrastructure firms for over 3,700 projects worth some US$372 billion through to 2028. These projects include airports, railways, hydropower plants, and digital infrastructure.

Halal food exports

The growing demand for global Halal products – especially food items – presents opportunities for the Halal food industry in the Philippines, enabling the industry to propel not only in Southeast Asia but also the wider international Halal goods market. Out of the US$2.6 trillion global Halal market, some 62 percent is accounted for food and beverages.

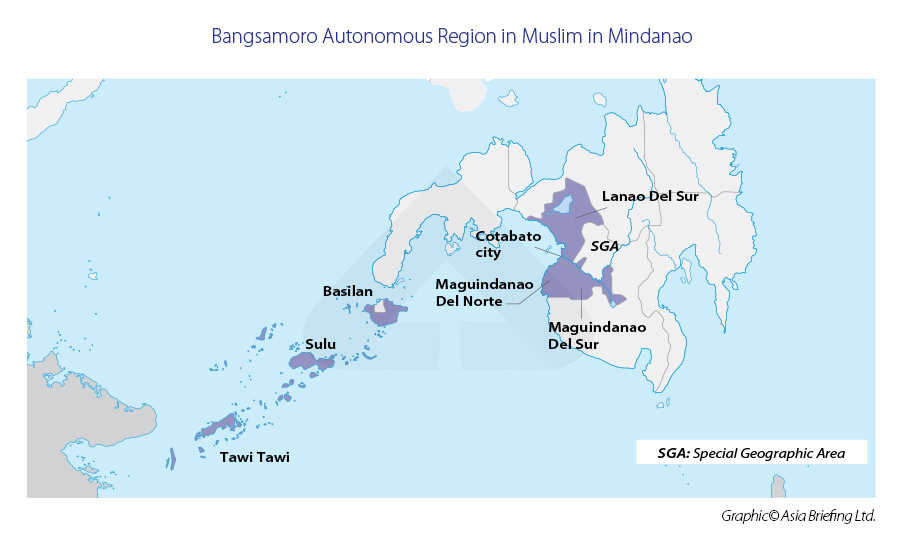

The Zamboanga City Special Economic Zone — a special economic zone located in Zamboanga City in Mindanao — is developing the Asian Halal Center, a 100-hectare estate that houses prospective manufacturers of Halal food. The Bangsamoro Autonomous Region in Muslim Mindanao (BARMM), an autonomous region in the Philippines has the largest concentration of Muslims in the country.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City, and Da Nang in Vietnam, in addition to Jakarta, in Indonesia. We also have partner firms in Malaysia, the Philippines, and Thailand as well as our practices in China and India. Please contact us at asean@dezshira.com or visit our website at www.dezshira.com.

- Previous Article A Guide to Withholding Taxes in Indonesia

- Next Article Unleashing Nickel’s Potential: Indonesia’s Journey to Global Prominence