Understanding Social Insurance in Singapore

The Central Provident Fund (CPF) is a social security savings scheme funded by contributions from employers and employees. This mandatory program is an important pillar of Singapore’s social security system and aims to meet the retirement, housing, and healthcare needs of its people.

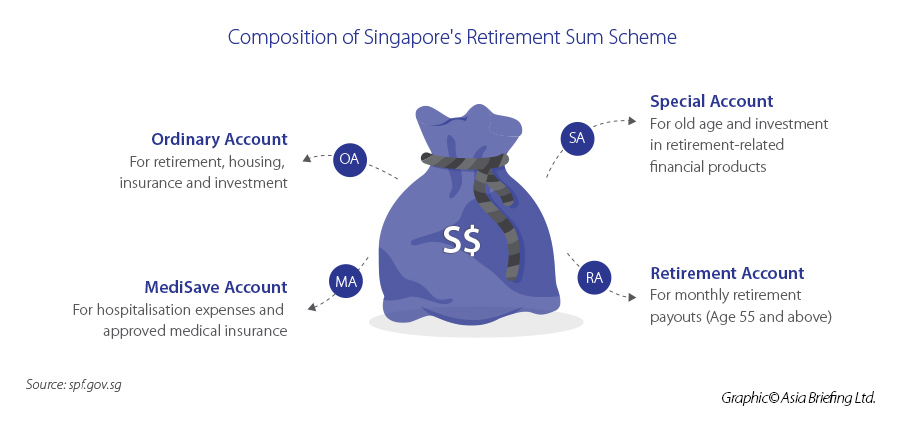

Individual CPF funds are further subcategorized into three savings accounts: Ordinary Account, Special Account, and Medisave Account.

The Ordinary Account can be used at any time to purchase a home, make investments, and provide for education. The Special Account cannot be utilized until the account holder reaches retirement, unless the money is used to purchase retirement-related financial products. This account will serve as the income a retired person receives.

The Medisave Account is used to pay for medical expenses, hospitalization expenses, and pay for approved medical insurance.

When a worker turns 55, savings from their Special and Ordinary accounts are transferred to their Retirement Account when they turn 55, at which point they can start withdrawing their savings. Workers begin to receive monthly payouts of their savings at age 65.

CPF earn risk-free interest on their savings. Interest rates vary for different CPF accounts and age groups and are updated on the CPF government website.

Employers can submit CPF contributions and make payments through the CPF EZPay system, which also automatically calculates the employer’s and employee’s contributions and updates the amount when the employer changes age group. A SingPass login is required for employers to make payments through CPF EZPay.

Amendments to the Central Provident Fund Act

On November 2, 2021, Singapore’s Parliament passed the amended Central Provident Fund (CPF) Act and the Retirement and Re-Employment Act.

Under these amendments, the government aims to streamline the CPF rules to offer greater flexibility for transfers and quicker disbursements and topping up of CPF accounts. Further, the retirement and re-employment ages will be raised to 63 and 68, respectively. Since 2017, Singapore employers are obligated to offer re-employment options for employees who reach the retirement age.

More ease for CPF members to receive retirement pay-outs

Retirement Sum Scheme (RSS) members who have depleted the funds in their Retirement Account (RA) will automatically have pay-outs from their Ordinary Accounts (OA) and Special Accounts (SA). This is to ensure there are no disruptions to pay-outs with the government aiming to implement this new rule in the first quarter of 2022.

Previously, RSS members who depleted their RA savings could only continue receiving pay-outs if they applied to transfer money in their OA or SA to their RA.

The RSS is one of two retirement schemes under the CPF Board, the other being CPF LIFE. The RSS provides CPF members with monthly pay-outs during retirement until the savings in their RA runs out, or they turn 90. CPF LIFE was introduced in 2009 and offers monthly pay-outs for life.

Simplifying tax relief rules

Under the Retirement Sum Topping-Up (RSTU) scheme, a CPF member can top up their SA (if they are below the age of 55) or RA (if they are 55 or above) via CPF transfer or cash. The CPF member can also top the SA or RA savings of their family members. There is also a S$7,000 (US$5,162) per year tax relief if a CPF member is topping up for themselves and an additional S$7,000 per year if they are top-up for parents, in-laws, grandparents, grandparents-in-law, spouse, and siblings.

Effective from January 1, 2022, the tax relief cap for voluntary top-ups will increase to S$8,000 (US$5,900) per year. In addition, the government has introduced a tax relief cap of S$8,000 per year to CPF members who top up a MediSave account (the account used for healthcare needs).

Quicker disbursement of CPF funds upon the death of a member

From April 2022, the duration in which the CPF funds are retained after death has been shortened to six months compared to the previous length of seven years. This timeframe gives beneficiaries enough time to claim nominated monies from the CPF Board.

Suppose a CPF member did not designate a CPF nomination. In that case, relatives can appoint a ‘beneficiary representative’ who can submit a consolidated claim for the funds at a maximum amount of S$10,000 (US$5,162). If there are disputes among the beneficiaries after the funds have been disbursed, the beneficiaries can seek recourse under the law.

Increase of retirement and re-employment ages

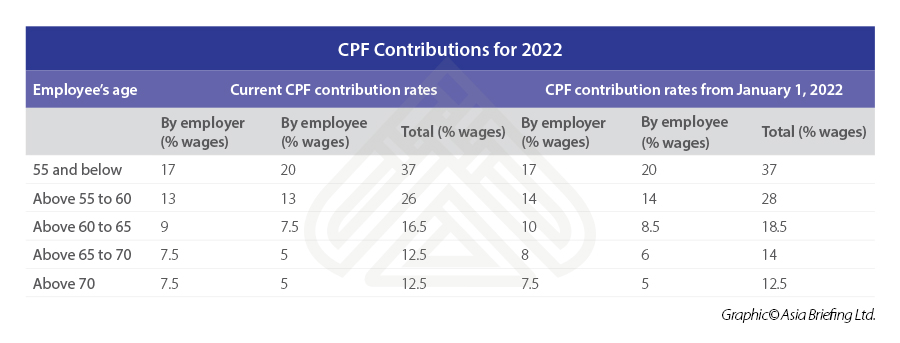

From July 2022, the retirement and re-employment ages will increase to 63 and 68, respectively, and 65 and 70 by 2030. Singapore’s Manpower Minister Tan See Leng told Parliament that the increase in the retirement and re-employment ages was necessary – particularly as by 2030, one in four Singaporeans will be 65 and older, resulting in talent shortages and hurting the country’s productivity and competitiveness. Businesses can raise their retirement and re-employment ages ahead of the scheduled timeline. In early 2021, the government announced that the CPF contribution rates for employees aged 55 to 70 years will increase earning more than S$750 (US$553) per month, starting from January 1, 2022.

Increase in CPF monthly salary ceiling

The CPF monthly salary ceiling will be increased in stages from September 1, 2023, to Jan 1, 2026.

The CPF is the obligatory savings and pension plan for Singaporeans and permanent residents that fund their retirement, healthcare, and housing needs in the country.

The increased ceilings will be implemented in four stages:

- September 1, 2023 – the monthly salary ceiling will be increased to S$6,300 (US$4,700);

- January 1, 2024 – the monthly salary ceiling will be increased to S$6,800 (US$5,072);

- January 1, 2025 – the monthly salary ceiling will be increased to S$7,400 (US$5,519); and

- January 1, 2026 – the monthly salary ceiling will be increased to S$8,000 (US$5,965);

This means that employees earning above the ceiling rate will take home a lower net salary – to set aside more for their CPF.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City, and Da Nang in Vietnam, in addition to Jakarta, in Indonesia. We also have partner firms in Malaysia, the Philippines, and Thailand as well as our practices in China and India. Please contact us at asean@dezshira.com or visit our website at www.dezshira.com.

- Previous Article How to Open a Corporate Bank Account in Singapore?

- Next Article A Guide to Personal Income Tax in Singapore