Thailand’s New Land and Building Tax Act

- Thailand’s new Land and Building Tax Act came into effect January 1, 2020; it was introduced in March 2019.

- The tax will be applied to residential, commercial, agricultural, and unused/vacant properties.

- The Act does provide a two-year transition period for property owners to adjust to the new law, during which period they will be subject to a reduced tax rate.

In March 2019, the Thai government introduced the new Land and Building Tax Act B.E. 2562, which has been in effect since January 1, 2020.

The Act obligates individuals, corporate entities, or any beneficiaries of land or buildings, to pay land and building tax. The new law replaces several legislations which include – the Land Tax of 1932; the Land Development Tax of 1965; the Notification of the National Executive Council No. 156 of 1972; and the Royal Decree Designating the Medium Price of Land for Land Development Tax Assessment of 1986.

The tax rates on properties were previously assessed on an income-based method. The Act replaces this method with an assessment based on the property’s appraised value, as determined under the current Land Code.

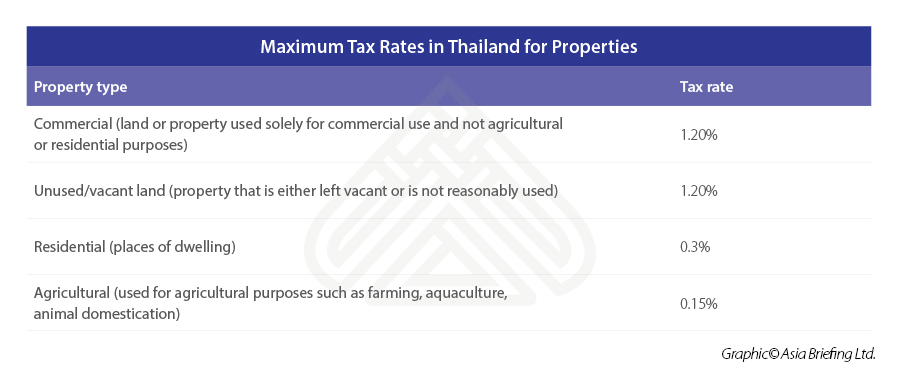

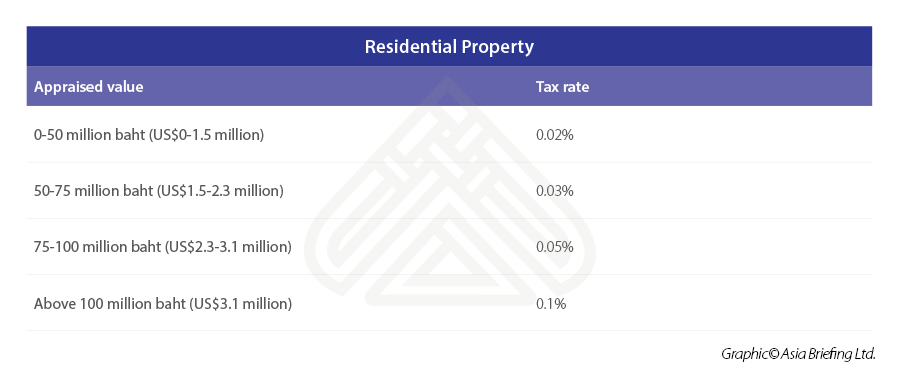

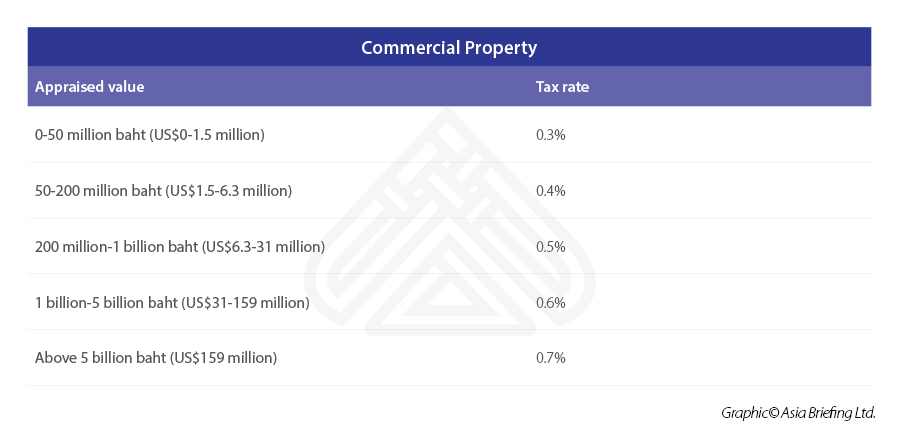

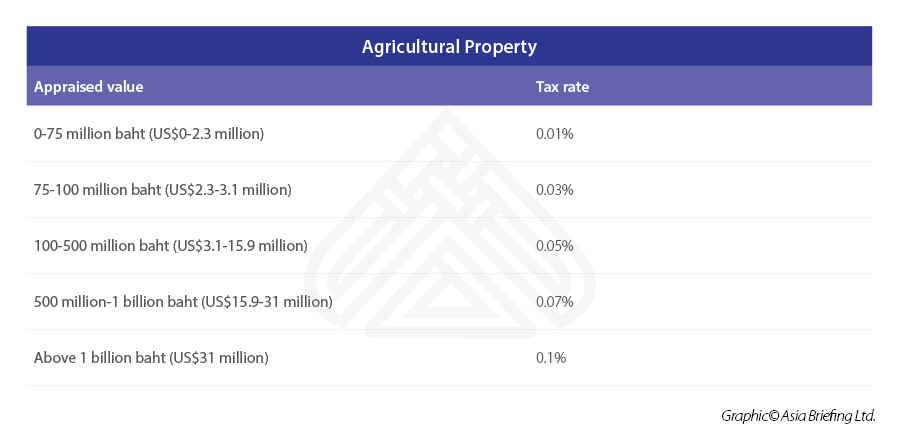

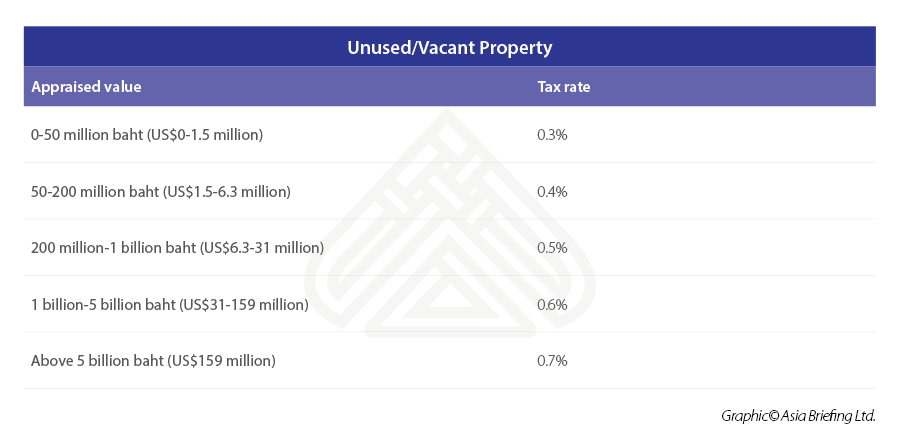

The tax will be applied to the following categories of property:

- Residential (including condominiums);

- Commercial;

- Agricultural; and

- Unused/vacant land.

Through these latest changes, the government hopes to introduce a progressive tax system, encourage landowners to utilize their land, and help reduce the overall tax burden on property owners. The tax payments will be due in April of every year.

Maximum tax rates for land and building tax

The Act sets a ceiling tax rate for the different categories of property.

Tax exemptions

Property owners can be exempted from the land and building tax if they fall under the following categories:

- Agricultural land worth up to 50 million baht (US$1.5 million);

- Land or building used for residential purposes and is worth up to 50 million baht (US$1.5 million) (the owner’s name should be on the deed of the property);

- The building is used for residential purposes and is worth up to 10 million baht (US$318,000) (the owner’s name should be on the deed of the property); and

- Individual owners of agricultural properties – they will be exempt from land and property tax for the tax period 2020-2023.

Transition period

The Act provides a two-year transition period, starting January 1, 2020, to allow property owners to adjust to the new law. During this period there will be a reduced tax rate. This can be seen from the following tables.

Tax reductions

There are further tax deductions in the broad tax deduction clause of the Act. To qualify, property owners should fulfil certain criteria:

For 50 percent tax reduction

- An inherited property that is used for residential purposes. The owner’s name must be on the deed; or

- Property used for energy infrastructure projects such as a power plant.

For 90 percent tax reduction

- Land or buildings that are under development for an industrial estate for no longer than three years;

- Land or buildings that are awaiting sale for no longer than two years starting March 2019;

- Land or buildings awaiting sale and is owned by a financial institution. The financial institution must have held the property for no more than five years;

- Land or buildings under development for industrial or residential purposes; or

- Land or buildings under development for an educational institute.

The government is estimated to collect 39.4 billion baht (US$1.2 billion) from land and property tax in 2020.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City and Jakarta. Please contact us at asia@dezshira.com or visit our website at www.dezshira.com

- Previous Article Indonesia and Singapore Sign Updated Double Taxation Avoidance Agreement

- Next Article Thailand Issues New Incentives for EEC