Thailand’s New Investment Promotion Policies Open a New Door to Foreign Investors

After 15 years of sticking to the same regulations, Thailand has finally declared that it will update its investment policy. The Thai Board of Investment (“BOI”) has announced a new seven-year investment promotion strategy, making significant changes to a number of BOI investment promotion policies. The new policies, which came into effect this year and will last until the end of 2021, aim to restructure the Thai economy to a more focused form of investment promotion.

The revised BOI policy is intended to create an attractive business environment for foreign investors with an emphasis on investment in the following six key sectors:

- Investment that enhances national competitiveness

- Activities that are environmentally friendly, save energy, or use alternative energy

- Clusters that create investment concentration based on regional potential and strengthen the value chain

- Investment in border provinces in southern Thailand that develop the local economy

- Special economic zones that create economic connectivity with nearby countries and prepare for entry into the ASEAN Economic Community

- Thai overseas investment to enhance the competitiveness of Thai businesses and Thailand’s role in the global economy

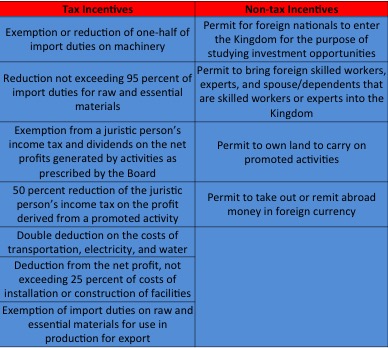

BOI Incentives

Under the new Investment Promotion Act (B.E. 2520), foreign investors in Thailand are granted a range of financial incentives and privileges; these include the following:

New Work Permit Regulations

According to the new Foreign Workers Act B.E. 2551, in certain cases foreigners do not need to obtain a work permit. These cases include: attending a meeting, purchasing goods in a goods exhibition, or making any visit to observe a business. These types of activities require a business visa (non-immigrant B visa). However, if the above activities exceed 15 days, a work permit is required.

Investment Incentives

Depending on the type of industrial project, the BOI is able to provide special privileges to projects that are expected to be highly beneficial to the country. The BOI encourages industrial development through two groups of investment incentives: Activity-based and Merit-based incentives.

RELATED: Thailand Economic Growth to be Curtailed in 2015, 2016 to be Brighter

RELATED: Thailand Economic Growth to be Curtailed in 2015, 2016 to be Brighter

Within Activity-based incentives, there are two groups:

- Group A (categorized into subgroups A1, A2, A3, and A4): business activities that use high-technology qualify for corporate income tax (CIT) incentives (for no more than eight years), machinery and raw materials import duty incentives, and other non-tax incentives.

- Group B (categorized into subgroups B1 and B2): business activities that use less complex technology qualify for machinery and raw materials import duty incentives and non-tax incentives.

The subgroups are arranged based on the importance of activities, with the top being most important.

All subgroups receive an exemption from import duty on machinery, a one-year of exemption of import duty on raw or essential materials used in manufacturing export products, and other non-tax incentives.

The Merit-based incentives aim to attract and stimulate investment and spending on activities that benefit the country or industry at large. The BOI grants these incentives based on the following:

- Merit on competitiveness enhancement: for projects that have investment or expenditures on:

- Research and development

- Donations to technology and human resources development funds

- IP acquisition/licensing fees for commercializing technology developed in Thailand

- Advanced technology training

- Development of local suppliers with at least 51 percent Thai shareholding in advanced technology training and technician assistance

- Product and packaging design.

- Merit on decentralization: for projects located in the 20 provinces with low per capita income, which will receive additional incentives.

- Merit on industrial area development: for projects located within industrial estates or promoted industrial zones. These projects will be granted one additional year of CIT exemption. However, the total period of CIT exemption will not exceed eight years.

Projects with activities in group A and group B may apply for merit-based incentives according to the conditions stipulated by the BOI.

BOI Promotion Criteria for Project Approval

The three BOI criteria for project approval are: development of competitiveness in the agricultural, industrial and service sectors; environmental protection; and minimum capital investment and project feasibility.

For the development of competitiveness in the agriculture, industrial, and services sectors:

- The value-added must be at least 20 percent of sales revenue (except for electronic products, agricultural produce, and coil centers, all of which must have value-added of not less than ten percent of revenue)

- Modern production processes and new machinery must be used. If old machinery is used, its efficiency must be certified by a reliable institution and BOI’s approval must be obtained

- A project with THB 10 million of capital investment must obtain a certification, such as ISO 9000, ISO 14000, or similar international standard certification within two years from the full operation start-up date, otherwise the CIT exemption will be reduced by one year.

In terms of environmental protection, systems must be installed for projects that may pose a threat to the environment. The BOI will consider the project’s location and prescribe the type of pollution treatment needed.

RELATED: Dezan Shira & Associates’ Tax and Compliance Services

RELATED: Dezan Shira & Associates’ Tax and Compliance Services

Finally, the requirements for minimum capital investment and project feasibility are as follows:

- The minimum capital investment requirement of each project is THB 1 million (excluding the cost of land and working capital) unless otherwise specified on the list of activities

- The ratio of debt-to-registered capital should not exceed three-to-one for a newly established project, while expansion projects will be considered on a case-by-case basis

- A project’s feasibility study must be submitted (as prescribed by the BOI) if the investment capital (excluding the cost of land and working capital) is more than THB 750 million.

Criteria for Foreign Shareholding

For projects in agriculture, animal husbandry, fisheries, mineral exploration and mining, and service businesses under List One of the FBA (B.E. 2542), Thai nationals must hold shares totaling at least 51 percent of the registered capital. However, foreign investors can hold a majority or all of the shares in promoted manufacturing projects stipulated in List Two and List Three of the FBA (B.E. 2542). Under certain circumstances, the BOI may set the maximum and the minimum for foreign shareholding in some promoted projects at the level it deems appropriate.

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email asean@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight. |

![]()

Tax, Accounting, and Audit in Vietnam 2014-2015

Tax, Accounting, and Audit in Vietnam 2014-2015

The first edition of Tax, Accounting, and Audit in Vietnam, published in 2014, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in Vietnam, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in Vietnam in order to effectively manage and strategically plan their Vietnam operations.

An Introduction to Tax Treaties Throughout Asia

An Introduction to Tax Treaties Throughout Asia

In this issue of Asia Briefing Magazine, we take a look at the various types of trade and tax treaties that exist between Asian nations. These include bilateral investment treaties, double tax treaties and free trade agreements – all of which directly affect businesses operating in Asia.

The 2015 Asia Tax Comparator

In this issue, we compare and contrast the most relevant tax laws applicable for businesses with a presence in Asia. We analyze the different tax rates of 13 jurisdictions in the region, including India, China, Hong Kong, and the 10 member states of ASEAN. We also take a look at some of the most important compliance issues that businesses should be aware of, and conclude by discussing some of the most important tax and finance concerns companies will face when entering Asia.

- Previous Article ASEAN Regulatory Brief: FATCA, GST, and a New DTA Protocol

- Next Article Norway Enters into Formal Partnership with ASEAN