Indonesian FDI Highest Among ASEAN Members in First Half of 2015

With growing uncertainty over China’s economic stability, recent FDI statistics released by the Financial Times come as a reassurance that investors are taking a more pragmatic, nuanced approach towards risk mitigation in Asia. First half inward investment figures illustrate investor confidence that profits can be made in areas less exposed to Chinese imports. Overall strong economic growth throughout ASEAN and India points to the fact that despite the Chinese slowdown, growth potential in Asia still exists.

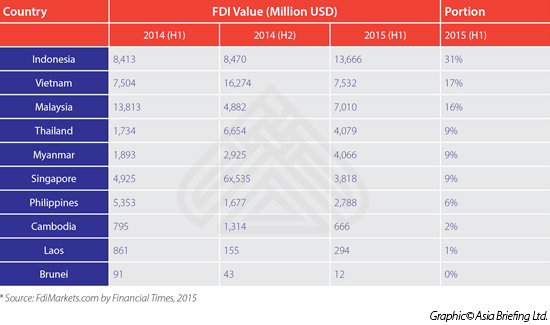

Among ASEAN members, those capturing the largest share of inward investment thus far this year are those least exposed to the stagnation of Chinese demand. Countries like Vietnam and Malaysia – whose large trade volumes with China promise to be offset by inclusion in the Trans Pacific Partnership (TPP) -elucidate this point. However, with upcoming elections in the USA and Canada, two large TPP members, concerns regarding further delays in TPP’s conclusion have cast a shadow over Vietnam and Malaysia’s growth prospects over the next few years.

Instead, Indonesia (absent from TPP negotiations) has managed to top the list, attracting 31% of FDI in ASEAN in the first half of 2015. With trade between Indonesia and China amounting to merely 7.5% of Indonesia’s GDP, compared to 18.8% and 16.2% for Malaysia and Vietnam, Indonesia promises investors opportunities to mitigate exposure to potential risks in China. As grounds for investment in Indonesia are much less speculative than its neighbors, a closer examination of current investment opportunities seems warranted.

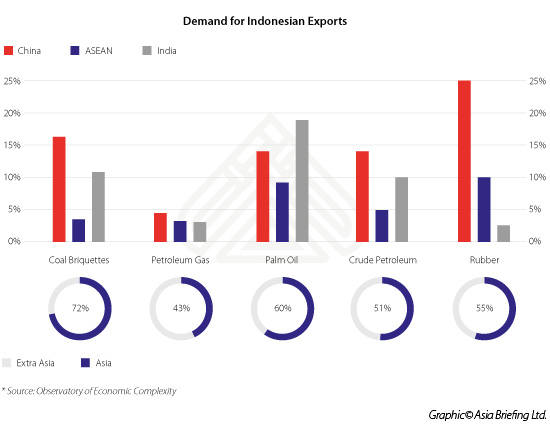

Despite the fact the fact that Indonesia enjoys the largest share of inward direct investment in ASEAN, the characteristics of its industries vary greatly. Top exports in Indonesia include coal, petroleum, palm oil, and rubber. While all industries have seen increased demand in the past years, the markets that these products are exported to, projected volatility in pricing, and the reception of these industries by Indonesian regulators play a significant role in their viability as investment destinations.

Looking first to demand for varying goods, the chart above explores imports of Indonesia’s top exports in China, India, and ASEAN. Large Chinese demand for goods such as rubber leave profitability contingent upon Chinese economic stability. Furthermore, the lack of demand for Indonesian exports in ASEAN and India prevents many Indonesian industries from taking advantage of the reduced trade barriers of the ASEAN Economic Community or providing a counterweight to a downturn in Chinese demand.

However, with high levels of demand from China, India, as well as ASEAN, palm oil shines through as an industry that is capable of simultaneously mitigating the risks of a Chinese slowdown and thriving in an increasingly profitable ASEAN marketplace. With Indian demand exceeding that of China, there is ample opportunity for exporters to shift gears in the event of lagging sales to the Chinese markets. Additionally, as the industry with the second highest level of demand among ASEAN member states, sales of palm oil should become more profitable as many of the non-tariff barriers within the region are removed with the implementation of the AEC.

In addition to shielding investors from risks in China, the general price stability of palm oil allows a greater degree of certainty with regard to projected returns on investment. Historical pricing data, coupled with projections for varying commodities in the next five years, paint a picture of stability for palm oil production. Given these low levels of volatility and limited exposure to China’s slowdown, palm oil is better positioned than most Indonesian exports to weather risks in Asian markets. Thus, in the coming years palm oil is projected to remain among the most stable of Indonesia’s top exports.

While geographically diverse demand and low levels of price volatility reduce risk for palm oil producers worldwide, the importance of Indonesian production cannot be overstated. Servicing 50% of global demand in 2014, and increasing exports by 30% since 2010, Indonesia’s business climate offers perfect conditions for investment. The labor intensive nature of palm oil production in particular allows Indonesian producers to leverage their relatively cheaper workforce against the more capital intensive nature of their competitor’s economies.

This is particularly true of Malaysia – Indonesia’s main competitor and a member of the ASEAN Economic Community (AEC). Although Malaysia currently has a competitive advantage in the more capital intensive downstream production of refined palm oil, the reduction of duties among AEC member states threatens to reduce margins associated with this line of production and erode its superior position visa vi Indonesia. The costs of these changes are already being realized – palm oil exports fell 3% in Malaysia between 2010 and 2014 – and can be expected to continue as the AEC is fully implemented in December of 2015. With reduced profit margins in its main competitor market, Indonesian production is perfectly positioned to capitalize upon its highly competitive workforce to service demand for palm oil in the ASEAN marketplace.

RELATED: Pre-Investment Services from Dezan Shira & Associates

RELATED: Pre-Investment Services from Dezan Shira & Associates

Government Regulations

A final consideration, and one of the utmost importance for any investment project, is the position of the host country towards FDI. Indonesia is no exception to this rule, with recent restrictions on foreign ownership in key industries highlighting the necessity of a strong understanding of the legal and regulatory environment within the country.

With regard to palm oil, there are several areas that should be of concern. First is the distinction between upstream Crude Palm Oil (CPO) and downstream refined products. Efforts to incentivize higher value added exports have resulted in a number of regulations and tax incentives that favor downstream production and stand to impact all investors in palm oil production. Additionally, certain locations within Indonesia have been prioritized by the Indonesian government for development and are subject to more favorable treatment by regulators.

Indeed, Indonesia, and the palm oil industry in particular, can offer investors a unique growth opportunity in ASEAN and a safe harbor from China’s slowdown and rising wages. However, given the imposition of past regulatory hurdles, it is important for investors to consult with a professional services firm in order to formulate how to best take advantage of this growth sector.

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email asean@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight. |

![]()

Tax, Accounting, and Audit in Vietnam 2014-2015

Tax, Accounting, and Audit in Vietnam 2014-2015

The first edition of Tax, Accounting, and Audit in Vietnam, published in 2014, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in Vietnam, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in Vietnam in order to effectively manage and strategically plan their Vietnam operations.

An Introduction to Tax Treaties Throughout Asia

An Introduction to Tax Treaties Throughout Asia

In this issue of Asia Briefing Magazine, we take a look at the various types of trade and tax treaties that exist between Asian nations. These include bilateral investment treaties, double tax treaties and free trade agreements – all of which directly affect businesses operating in Asia.

The 2015 Asia Tax Comparator

In this issue, we compare and contrast the most relevant tax laws applicable for businesses with a presence in Asia. We analyze the different tax rates of 13 jurisdictions in the region, including India, China, Hong Kong, and the 10 member states of ASEAN. We also take a look at some of the most important compliance issues that businesses should be aware of, and conclude by discussing some of the most important tax and finance concerns companies will face when entering Asia.

- Previous Article Asian Highway to Link India, Myanmar, and Thailand

- Next Article Eurasian Economic Union (EAEU) plans FTA expansion within ASEAN