Indonesia’s Omnibus Law: New Tax Treatment to Support Ease of Doing Business

Indonesia’s Omnibus Law continues to impact the business, tax, and regulatory landscape. In this article, we note new income tax exemptions for dividend and offshore income in Indonesia as well as reduced withholding tax rate on bond interest, taxation of foreigners, and VAT treatment during the pre-production period.

Indonesia introduced Government Regulation 9 of 2021 (GR 9/2021) and its implementing regulation under the Ministry of Finance Regulation 18 0f 2021 (PMK 18/2021) in February 2021 that makes amendments to the country’s income tax law, and value-added tax law (VAT).

The two regulations aim to provide a relaxation of income tax and a more business friendly approach to VAT, among others, as the government continues to reform the tax system to support the ease of doing business in Indonesia.

These regulations are part of the 76 or so amended regulations initiated by Indonesia’s Omnibus Law, which represents the first time in the country’s legal history where such extensive amendments have been made through a single legal instrument.

Tax under Indonesia’s Omnibus Law

Criteria for domestic tax subjects

Under Indonesia’s previous income tax law, an individual is considered a domestic tax subject if they were present in the country for more than 183 days during a 12-month period, or they have an intention to stay in Indonesia.

PMK 18/2021 has provided further clarification on the definition of ‘residing in Indonesia’ and the ‘intention to stay in Indonesia’.

‘Residing in Indonesia’ is defined as an individual who:

- Lives at a place of residence in Indonesia that is at their disposal and can be accessed at all times, which they own, rent, and is not a place of transit;

- Have their vital interests in Indonesia;

- Have their habitual abode in Indonesia.

An ‘intention to stay in Indonesia’ needs to be substantiated with the following documents:

- A permanent stay permit;

- A limited stay visa;

- A limited stay permit; or

- Other documents that support their stay of more than 183 days in Indonesia.

Territorial taxation for foreigners

Foreigners who have become domestic tax subjects will only be taxed on Indonesian-sourced income. This is only applicable if they meet the expertise requirements from Appendix II of PMK-18.

Their expertise, however, must be supported by:

- A certificate issued by a government-authorized institution, or have a minimum of five years work experience in the field of science, technology, and math; and

- An obligation for knowledge transfer to an Indonesian citizen.

The territorial tax treatment is available for four years of residency. If the foreign individual leaves Indonesia and re-enter Indonesia within the four-year period, the territorial taxation will begin from the time they first became a domestic tax subject.

Foreigners looking to apply for the territorial tax treatment must do so through the Directorate General of Taxes (DGS). Those who were already a domestic tax subject prior to the issuance of PMK-18/2021 can also apply to the DGS for this tax treatment. If approved, the territorial taxation will start from November 2, 2020.

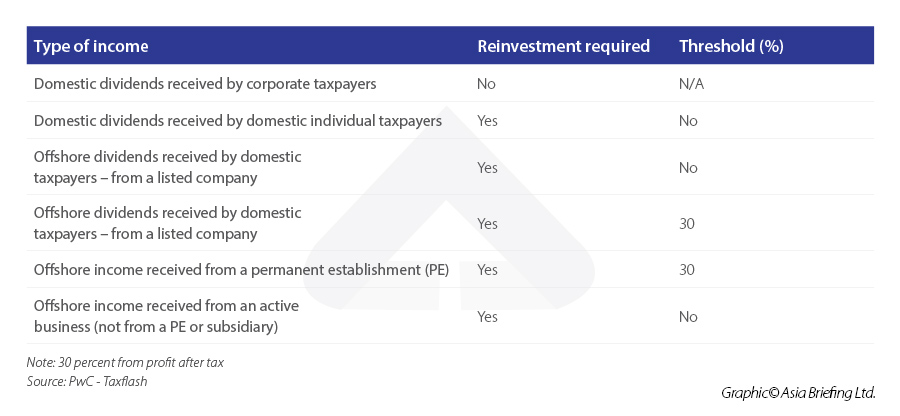

Dividends and offshore income exempted from income tax

To increase investments in Indonesia’s financial markets and the real sector, the government has provided income tax exemptions for foreign dividends received by domestic taxpayers. The reinvestment requirements is not required for domestic dividends received by domestic corporate taxpayers.

Such concessions will require reinvestment for a certain period from when the dividend is received. PMK-18/2021 provides details on these reinvestment requirements:

Qualifying reinvestments are as follows:

- Investment in financial market instruments such as:

- Government bonds, including shariah instruments;

- Bonds or sukuk issued by a state-owned enterprise, private companies;

- Financial investments in perception banks including shariah banks; or

- Other legal forms of investments.

Investments in financial instruments outside the money market include:

- Investment in real sector;

- Investment in infrastructure through a private-public partnership;

- Equity cooperation in an already existing company domiciled in Indonesia;

- Cooperation with the Indonesian Sovereign Wealth Fund; or

- Lending to small and medium-sized businesses in Indonesia.

The investment must be held for a minimum of three years from when the dividend or offshore income is received. The taxpayer must also invest he dividend or offshore income in the qualifying investments by the end of the third or fourth month after the end of the fiscal year. Finally, the investment cannot be transferred except to another qualifying investment.

If the reinvestment requirement provides a 30 percent threshold, the taxpayer can enjoy the full exemption if this threshold is fulfilled. However, if the reinvestment is less than the 30 percent threshold, the taxpayer must pay income tax on the spread between the investment amount and the 30 percent threshold to enjoy the exemption.

Investors should note that the exemption does not apply to foreign citizens who utilize the double tax avoidance agreement (DTA) between Indonesia and the partner country/jurisdiction of the DTA.

Reduced withholding tax rate on bond interest

Under GR 9/2021, the government has reduced the withholding tax (WHT) rate for bond interest paid to non-residents from 20 percent to 10 percent.

This lowered rate applies to all types of income treated as bond interest, which includes capital gain and has been effective since August 2, 2021.

Value-added tax under Omnibus Law

VAT during pre-production period

Before the Omnibus Law, if a VAT-able entity had not moved beyond the pre-production stage (not exported or delivered any VAT-able goods or services) during a certain period of time, then the entity is deemed to have failed to produce any ‘input VAT’ that has already been credited and thus can no longer be claimed.

PMK-18/2021 emphasizes this point and that a VAT-able entity is considered to not have made a delivery if they have not exported or delivered any VAT-able services or goods. Any deliveries made for the entity’s own use, or as gift for customers, or deliveries from a head office or branch office, are not considered as deliveries when assessing if an entity has moved beyond the pre-production stage.

The pre-production stage is generally three years, which is extended for manufacturing sectors and businesses sectors under the National Strategic Projects to five or six years, respectively.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City, and Da Nang in Vietnam, Munich, and Esen in Germany, Boston, and Salt Lake City in the United States, Milan, Conegliano, and Udine in Italy, in addition to Jakarta, and Batam in Indonesia. We also have partner firms in Malaysia, Bangladesh, the Philippines, and Thailand as well as our practices in China and India. Please contact us at asia@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Strengthening Myanmar’s Trade Relations with Bangladesh

- Next Article Cambodia Ratifies Free Trade Agreement with China