German FDI in ASEAN Part I: Brunei and Cambodia

The Association of Southeast Asian Nations (ASEAN), featuring ten dynamic and growing economies, has become increasingly favorable for foreign investment in recent years. This is mainly due to the desire of governments in ASEAN countries to promote FDI and the increasingly growing domestic markets in the region. The ongoing Sino-US trade war, the creation of the ASEAN Economic Community in December 2015, and the streamlining of ASEAN’s regulatory landscape greatly improved the attractiveness of the region for investors.

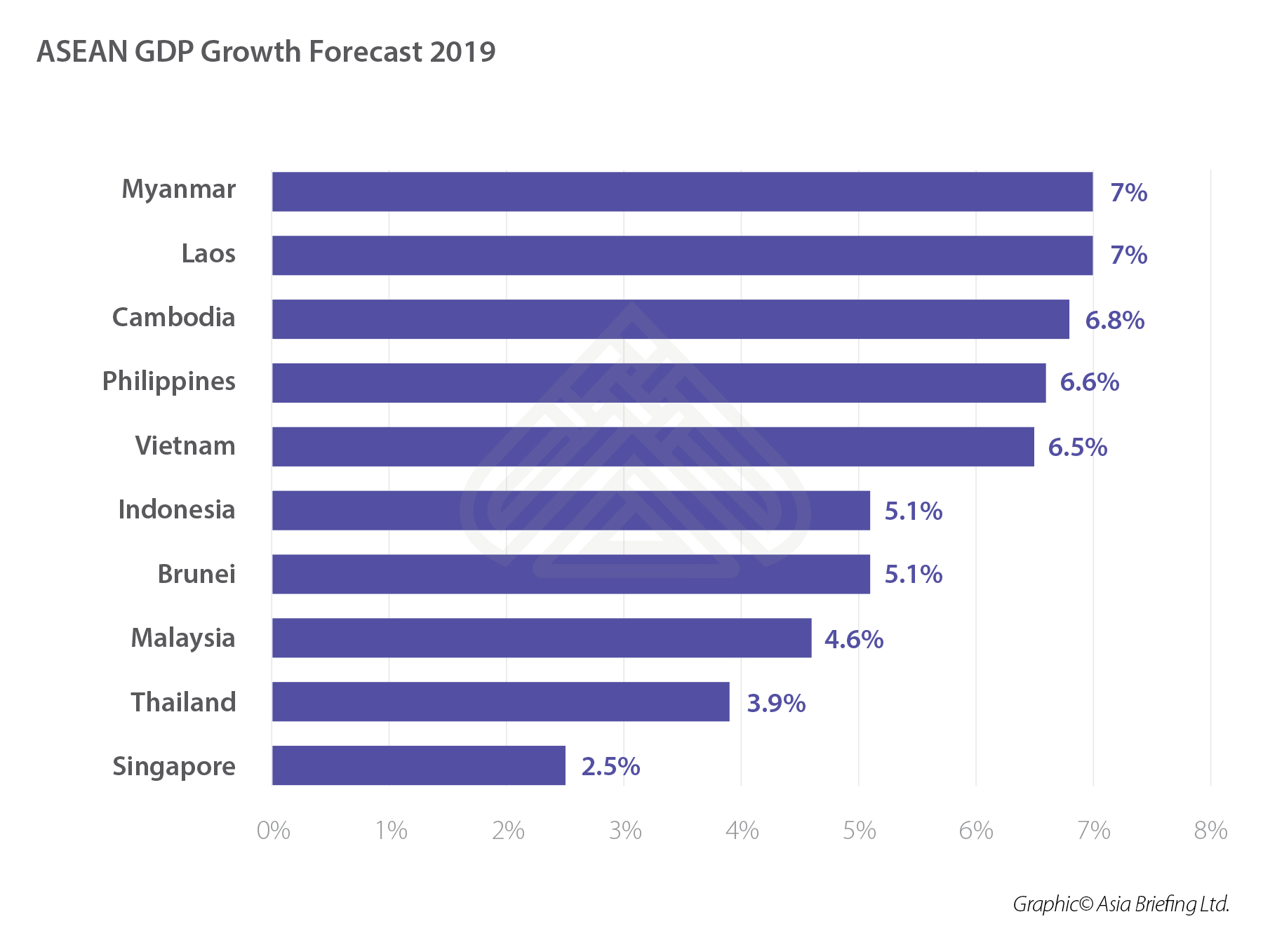

In particular, the manufacturing sector benefits largely from FDI as several ASEAN states are able to position themselves as an alternative to China. Cheaper wages and an advantageous geographical location between the Chinese and European markets makes ASEAN increasingly attractive. The outlook for the ten ASEAN countries is vastly positive. Barring Singapore which is already an industrialized high income economy, all other ASEAN states are expected to grow between 4 percent and 7 percent in 2019.

German investment in ASEAN has been increasing steadily and has the potential to grow further in the coming years.

In order to understand German investment in the region a closer look at FDI flows into each individual ASEAN state is necessary. In the first part of this four-part article, we look at Brunei and Cambodia.Brunei

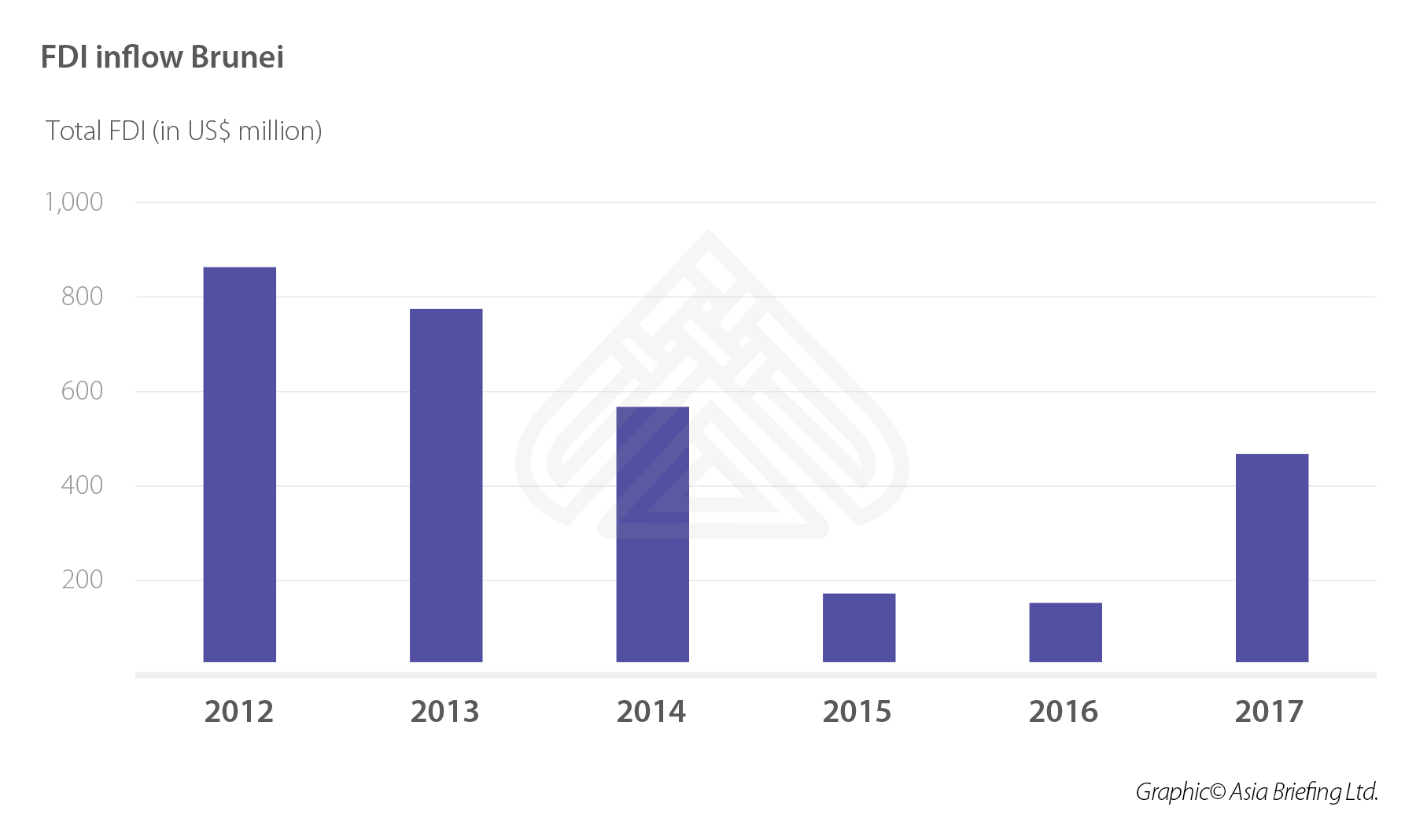

Brunei represents one of the most developed countries within ASEAN. Claiming one of the top rankings in the World Bank’s Ease of Doing Business Index, the country is placed at the first position in terms of ease of securing credit. Considering the size of the country, FDI inflows have played a major role in its economic development. However, German FDI did not play a very major role in Brunei in recent years.

Germany – Brunei relations at a glance

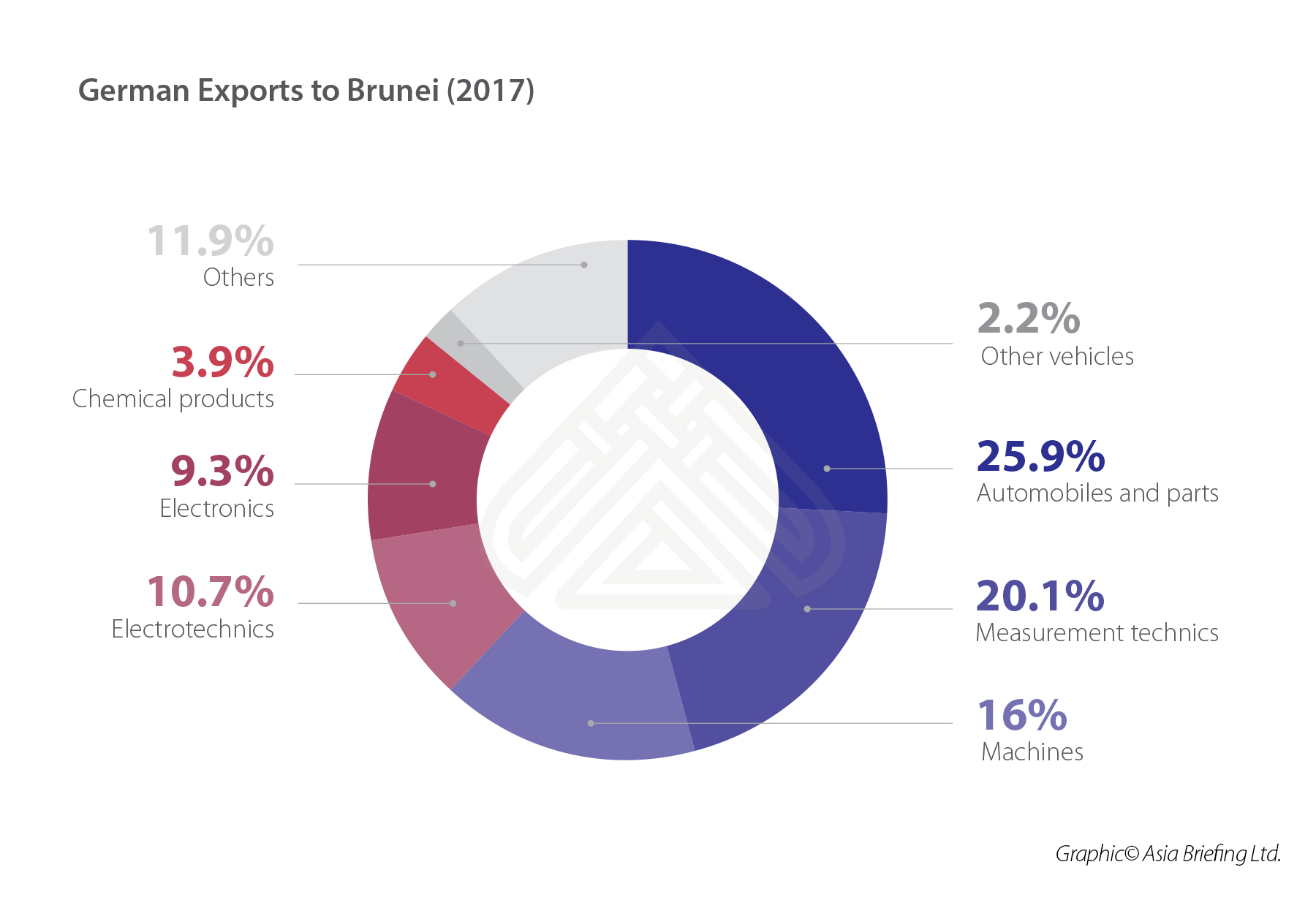

German exports to Brunei decreased from US$170 million in 2015 to US$57 million in 2017. Imports from Brunei declined due to slowing exports in the oil and gas sector. However, a particularly high demand for machinery from Germany is fuelling an increase of German exports to Brunei in recent years.

Several German companies have already established a business presence in Brunei. Heidelberg Cement has been present since 2000 supplies 65 percent of the construction market in Brunei. ThyssenKrupp is currently engaged in the construction of a major fertilizer plant in Brunei to support local efforts to diversify the economy. Siemens which is involved in Brunei since 1972, is currently studying the government’s effort towards digitalization and is expecting to make large investments in the coming years.

Brunei’s Investment Outlook

Brunei’s economy has faced challenges due to fluctuations in the oil and gas sector in recent years. In 2018, higher exports of Liquified Natural Gas (LNG) have given the export sector a boost with a 2.3 percent GDP growth that is expected to increase in 2019 to over 5 percent.

With the government’s diversification plans to decrease the dependence on the natural resources sector and increase innovative and technology-oriented businesses, Brunei opens up vast opportunities for German investments. With a largely well-educated and English-speaking population as well as an FDI friendly environment, Brunei represents a perfect investment opportunity for Germany.

The majority of German projects aim at developing high-technology and trade in Brunei and to use the special geographic location of the nation. Brunei is not yet comparable with Singapore but with the increasing lack of space and high costs in Singapore, Brunei could offer a potential alternative for high-tech companies and logistics firms.

Wawasan Brunei 2035

Wawasan Brunei 2035 is a development framework first announced in 2004. It shall position the country amongst other top nations in the world in term of high education and income. The strategy is that Brunei is recognised everywhere for the accomplishments of its well-educated people, the quality of life and its dynamic, sustainable economy.

The project is built upon attracting more FDI and growing local businesses. Promotion of the halal industry with the Bio Innovation Corridor, innovation and technology and creative industry, cotton industry and cooperatives are already implemented. The Ease-of-Doing Business Unit was set up to further improve Brunei’s already advance commercial climate – the country is currently one of the top nations on the Ease of Doing Business Index.

A large part of the initiatives focus on digitalization of the public sector especially under the Digital Government Strategy 2015-2020. Increasing public-private collaboration, information exchange and transparency are the main objectives. This will enable smooth communication amongst the 86 percent of the population using the Internet in Brunei – the highest ratio of all Southeast Asian nations.

The government aspires to implement national standards and accreditations in line with the best international practices. Darussalam Enterprise was set up, which aims at promotion entrepreneurial spirit and facilitating companies with growth visions.

Pulau Muara Besar Project

Another major project in diversification of the national economy is the Pulau Muara Besar Project. It is a large-scale development project for a deep-water harbour and industrial complex on more than 900 hectares of land. An attached business and commercial area is included as well.

In terms of Brunei’s location in the middle of ASEAN and alongside the major trading routes from East Asia over the Middle East to Europe, this project can catapult Brunei to a centre of attraction for logistics firms transporting goods from East Asia to Europe.

Risk analysis

Due to the high export dependency of the oil and gas sector,the country’s GDP growth largely depends on this sector.

Despite the vastly growing demand for LNG of 8.5 percent in 2018, 86 percent of the world LNG demand comes from Asian markets. Brunei therefore needs to tackle challenges to further compete in this market.The population is largely skilled and English-speaking but on the other hand with an overall small population, this represents a potential problem. Firms looking to set up in Brunei need to “import” their workers which could make business activities more expensive.

Cambodia

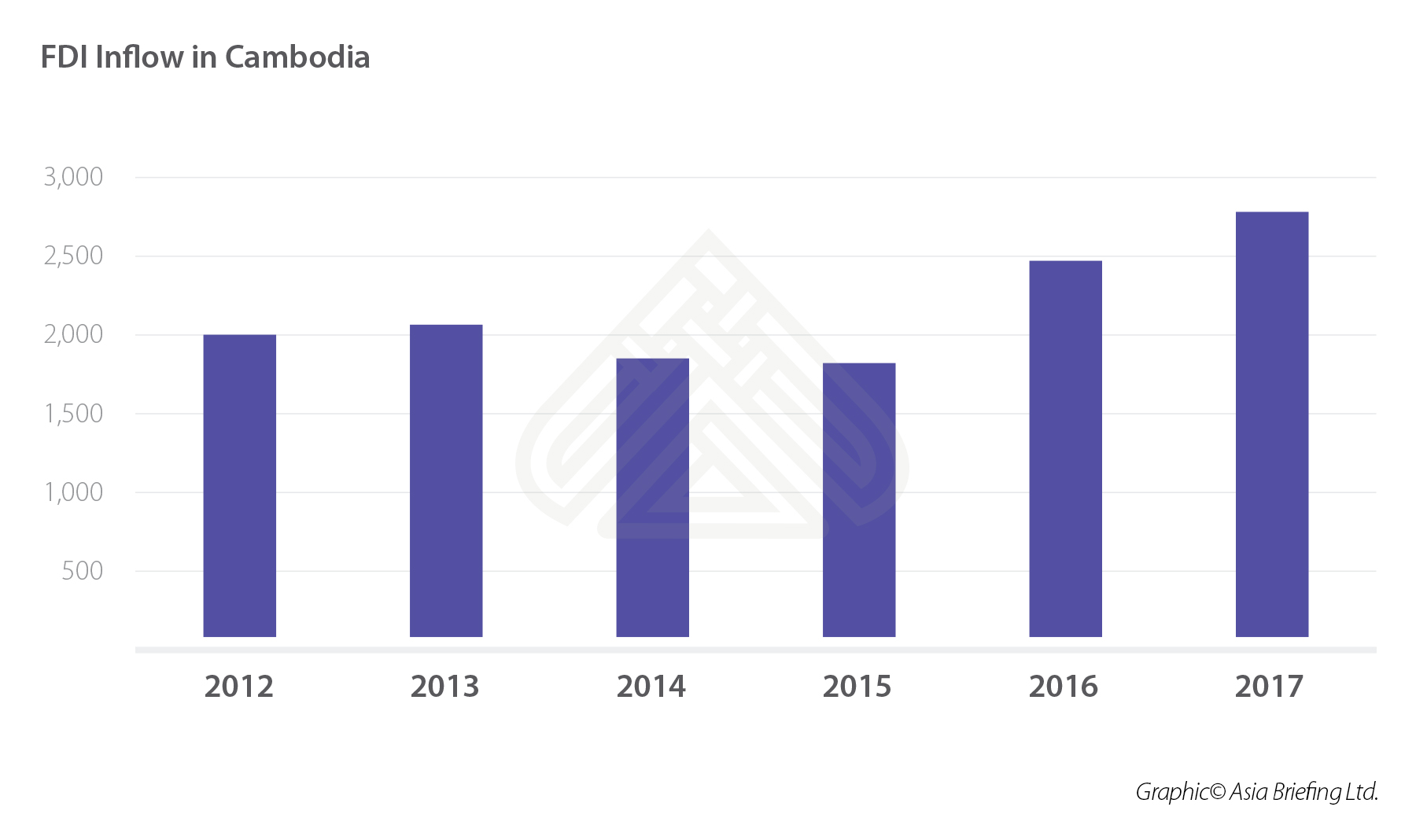

Situated in the middle of ASEAN with a steady growth, Cambodia represents a country on the move. Ranked 37 on the Market Potential Index 2018, the country opens up several investment opportunities as indicated below. As far as overall FDI inflows are concerned, German FDI plays only a minor role so far. The strategic location between Vietnam and Thailand – two major drivers of ASEAN economic development – open Cambodia as a supplier and support base for industries in these countries that require cheaper workers.

Germany – Cambodia Relations at a Glance

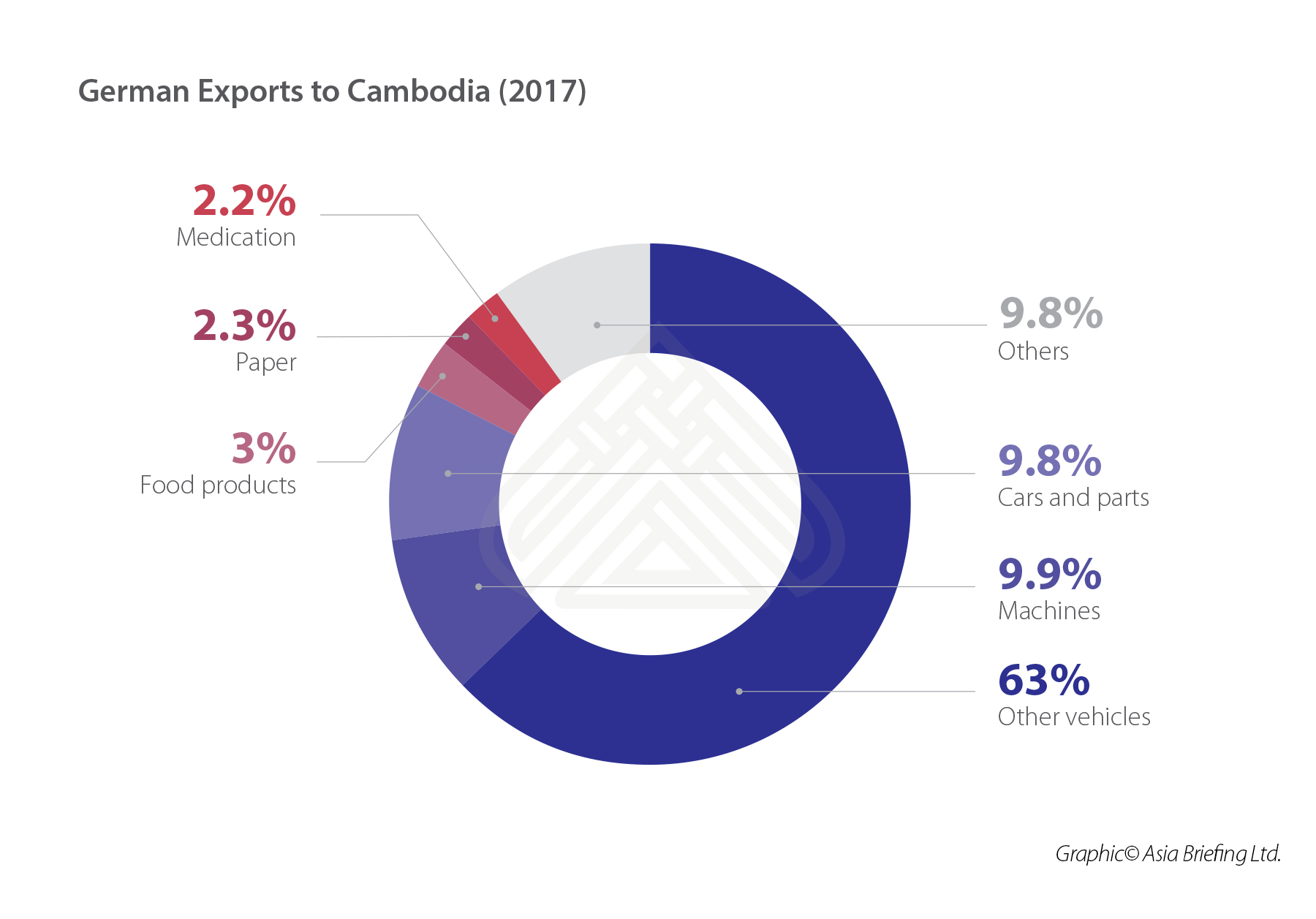

German imports from Cambodia are largely confined to textiles (74.9 percent) and footwear (12.5 percent). The Balance of exports and imports is negative from a German point of view. In 2017, Germany imported US$1,742 million worth of goods from Cambodia while exporting only US$ 286.7 million. Imports and exports increased in the recent years, although Cambodian imports from Germany increased slightly while exports rose to nearly 160 percent between 2015 and 2017.

Cambodia is relatively less attractive for German firms as it is located between Thailand and Vietnam where several German companies have already established regional headquarters and production facilities. Despite this, the option of investing in Cambodia has increasingly drawn the attention of German companies owing to the country’s low wages and proximity to manufacturing sites in Thailand opens. This opens up opportunities for the setting up of supplying and supporting industries in Cambodia. DEG, a German engineering company, expanded their operations to Cambodia recently. In 2017, InSITE Bavaria signed a Memorandum of Understanding (MoU) with Cambodia based Worldbridge Logistics to conduct a feasibility study on a German-Cambodian technology cluster.

Cambodia’s Investment Outlook

As German brands have a good reputation in Cambodia and with increasing preferences for higher lifestype products by a growing middle income consumer class, further opportunities are likely to open up for German firms in Cambodia. Providing an annual growth rate of over 6 percent and with several investment incentives, Cambodia is a vastly unexplored territory for German investors.

In particular, the pharmaceutical sector offers growing opportunities for German exporters. Growing income and a higher average age has in recent years led to an increase in demand for medical equipment and pharmaceuticals. Especially with the ratification of the ASEAN Medical Device Directive, a law to unify standards amongst ASEAN countries, the market opens not only in Cambodia but in the entire ASEAN.

The growing tourism, transportation and logistics sector also open up opportunities. The government plans to establish more Special Economic Zones, especially along the Thai border. These SEZs open up the possibility for supporting industries to be set up and supply factories in Thailand while benefiting from the cheap wages in Cambodia.

With an annual increase of around 20 percent over the last few years, the energy sector presents major opportunities for German investors. The Generation Development Plan 2016-2025 aims increases of 2.84 GW spread over several supply fields from fossil over water to solar power.

For further development of its exports-focused economy, Cambodia requires massive investments in infrastructure. Investments to the tune of US$500 million annually are estimated for the development of roads, railways, and harbors. A large part of this capital is expected to be generated by FDI.

Risk analysis

Despite the opportunities in Cambodia, there are still major challenges that require the government’s attention. The above-mentioned lack of infrastructure makes investments difficult outside of the several SEZs in which the infrastructure is relatively better. These zones provide the opportunities to build on reliable infrastructure, located close to other markets and the opportunities to take suppliers directly into the SEZ.

A further obstacle in Cambodia is the lack of qualified individuals. No comprehensive government scheme for the establishment of skills-based education system is in place. Skill development is largely provided by private operators. Although in Thailand and Vietnam, German organizations have already successfully established skill development programs, this could increasingly become an option for them in Cambodia.

In the second part of this five-part article, we will look at German FDI in Indonesia and Laos.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City and Jakarta. Please contact us at asia@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Les perspectives d’investissement à Singapour pour 2019

- Next Article Cambodia’s Investment Outlook for 2019