Evaluating Cambodia’s Tax Reform

By Dezan Shira & Associates

Editor: Alexander Chipman Koty

Cambodia’s updated Law on Financial Management for 2017 reflects the government’s ongoing efforts to revamp the country’s tax system and bring more businesses operating in the informal sector into the formal tax regime by offering incentives for small taxpayers. The amended laws, which came into effect on January 1, offer lower tax rates for small and medium sized enterprises and tax exemptions for firms that uphold quality accounting. The new rules continue a tax reform initiative that began in 2013 to increase the government’s tax revenue collection capabilities and better regulate Cambodia’s significant informal economy. Successful implementation will better equip foreign investors to compete with domestic firms in the informal sector that are able to offer lower rates for their services by avoiding tax obligations.

An uneven playing field

Although on paper Cambodia’s laws are open and conducive to foreign investment, in practice the country’s business environment presents considerable challenges for overseas entrants. Foreign investors operating in Cambodia generally adhere to written laws and compliance requirements, and pay the relevant taxes. However, the government has long struggled to absorb a sizeable portion of the domestic economy into the real tax paying regime, which creates an uneven distribution of tax burdens.

In early 2016, an amendment to the Law of Taxation eliminated the Estimated Tax Regime (ETR), representing one of Cambodia’s most significant tax reforms in years. Those operating under Cambodia’s real tax regime faced an uneven tax burden compared to those under the ETR, with obligations including a 10 percent withholding tax on rent, a salary tax ranging from zero to 20 percent, a profit tax of 20 percent, and the requirement to charge customers 10 percent VAT for supplying goods and services. In contrast, under the ETR, small taxpayers outside the formal regime were able to negotiate their liabilities with collectors based on estimations of their monthly estimated tax, which normally came to around two percent. Further, real regime taxpayers had to pay an addition 15 percent tax on services provided by unregistered taxpayers, giving legitimate taxpayers an additional burden.

While the ETR was designed to encourage small taxpayers in the informal regime to pay taxes by taking a more flexible approach that did not require formal accounting and bookkeeping, in practice it discouraged firms from entering the real tax system. ETR payers would pay a far smaller tax burden than real regime payers, so they had little incentive to formally register. Those who were not actually genuine small taxpayers often underreported income or avoided registration to skirt tax obligations. Further, the system encouraged corruption, as collectors could charge bribes in exchange for a low tax assessment. Indeed, Cambodia’s high levels of corruption – it was ranked 150 out of 168 countries by Transparency International – lead to bureaucratic inefficiencies and unexpected costs. According to the Phnom Penh Post, about 60 percent of the General Department of Taxation’s resources were spent collecting less than one percent of tax revenue.

![]() RELATED: Tax Compliance Services from Dezan Shira & Associates

RELATED: Tax Compliance Services from Dezan Shira & Associates

Recent tax reforms

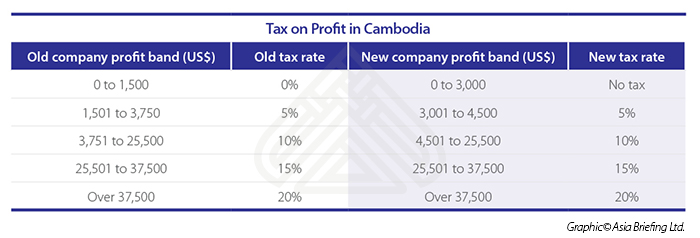

The amendment to the Law of Taxation consolidated taxpayers into a three-tiered system for small, medium, and large taxpayers. Small taxpayers are defined as sole proprietorships with annual turnover of US$65,000 to US$175,000; medium taxpayers are enterprises with annual turnover between US$175,000 and US$500,000; and large taxpayers are those exceeding US$500,000 or registered as a Qualified Investment Project. The government also introduced a number of tax exemptions and incentives to ease the burden of firms transitioning into the formal tax system, such as reduced VAT obligations. For example, small taxpayers do not have to pay the additional 15 percent on services provided by unregistered taxpayers. The government also created a progressive Tax on Profit regime to encourage more small and medium sized taxpayers to enter the formal tax system. Rather than a flat 20 percent company profit tax, the progressive tax works on a sliding scale based on profit size. Profit tiers were recently updated to further reduce the small taxpayers’ obligations and encourage them to formally register.

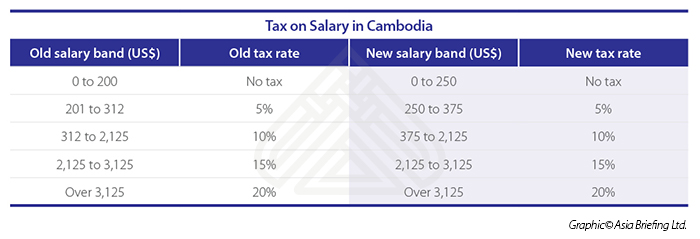

Along with the new progressive tax rates, which mainly target firms with small margins, the updated provisions include new monthly Tax on Salary brackets for employees. Like the progressive tax rates for company profits, the new Tax on Salary rates are designed to alleviate the tax burdens on the lowest earners.

In addition to the updated bands and rates for both companies and employees, several other measures have been put in place to ease tax requirements for small and medium sized payers in order to develop a more formalized economy. For example, firms can qualify for an exemption from Minimum Tax (MT), which is one percent of annual turnover of all taxes aside from VAT, if the firm maintains a proper record of accounts and has its financial statements externally audited. The government is also instituting a ranking system to reward taxpayers that comply with their mandated tax obligations, such as by meeting deadlines for tax returns and maintaining the requisite legal documents. On the 20 point scale, 10 points or less earns a bronze rating, 11 to 15 points a silver, and 16 or more a gold. While the specific incentives for attaining higher ratings have not yet been announced, they are representative of the government’s ongoing efforts to encourage firms to properly pay taxes.

![]() RELATED: The Guide to Corporate Establishment in Cambodia

RELATED: The Guide to Corporate Establishment in Cambodia

Going forward

Cambodia’s tax reforms appear to be slowly helping the country develop a more rigorous and formalized tax system, and thereby create a more efficient and predictable business environment. Through the first 10 months of 2016, the Cambodian government collected US$1.3 billion in taxes – a 21 percent increase over the previous year, and far higher than the paltry US$600 million collected in 2006. The World Bank predicts tax revenue to account for 18.8 percent of Cambodia’s GDP in 2016, compared to just 10 percent in 2011. Foreign investors and the rest of the formal business sector have long complained about the uneven playing field when competing with players in the informal sector who shirk laws and obligations to gain price point advantages on goods and services. Additionally, as the Cambodian government receives more tax dollars, it has more resources at its disposal to invest in areas such as infrastructure, education, and environmental protection. If properly invested, these funds could be used to spur the country’s growth and benefit all businesses operating in the country.

However, Cambodia’s efforts at comprehensive tax reform are still far from complete. Although the government aims to integrate the informal sector into the formal taxpaying sector of the economy through various incentives, many taxpayers are hesitant to make the leap. Not only are many small taxpayers distrustful of the government and fearful of exposing themselves to extortion from corrupt officials, but simply paying taxes can be an intimidating task, particularly given that lower level officials often are not completely aware of the exact regulations themselves. Paying taxes in Cambodia requires 40 payments per year, which is almost double the average in the East Asia and Pacific region and nearly quadruple compared to OECD countries. Even those in the formal economy often struggle to fully comply – for example, although registered businesses are now required to register online, Cambodia’s Commerce Ministry revealed that fewer than half of them had done so. That being said, for what can still be considered a frontier market at a low level of development, Cambodia has made significant progress in developing a streamlined business environment, and its recent tax reforms are another step in this direction.

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email asean@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight. |

![]()

Annual Audit and Compliance in ASEAN

For the first issue of our ASEAN Briefing Magazine, we look at the different audit and compliance regulations of five of the main economies in ASEAN. We firstly focus on the accounting standards, filing processes, and requirements for Indonesia, Malaysia, Thailand and the Philippines. We then provide similar information on Singapore, and offer a closer examination of the city-state’s generous audit exemptions for small-and-medium sized enterprises.

The 2016/17 ASEAN Tax Comparator

The 2016/17 ASEAN Tax Comparator

In this issue of ASEAN Briefing, we examine regional taxation in ASEAN through a comparison of corporate, indirect, and withholdings taxation. We further present an overview of the compliance environments found across the region and analyze ASEAN’s tax environment in the context of the time and documentation required in each country.

Human Resources in ASEAN

Human Resources in ASEAN

In this issue of ASEAN Briefing, we discuss the prevailing structure of ASEAN’s labor markets and outline key considerations regarding wages and compliance at all levels of the value chain. We highlight comparative sentiment on labor markets within the region, showcase differences in cost and compliance between markets, and provide insight on the state of statutory social insurance obligations throughout the bloc.