Tax Obligations of Non-Profit Organizations in Singapore

There are specific tax obligations and incentives that are on offer for non-profit organizations (NPOs) in Singapore.

Charity Status or status as Institution of Public Character (IPC) provides NPOs with additional advantages. Nonetheless, to be treated under these schemes an organization needs to apply to the Singapore authorities after establishment.

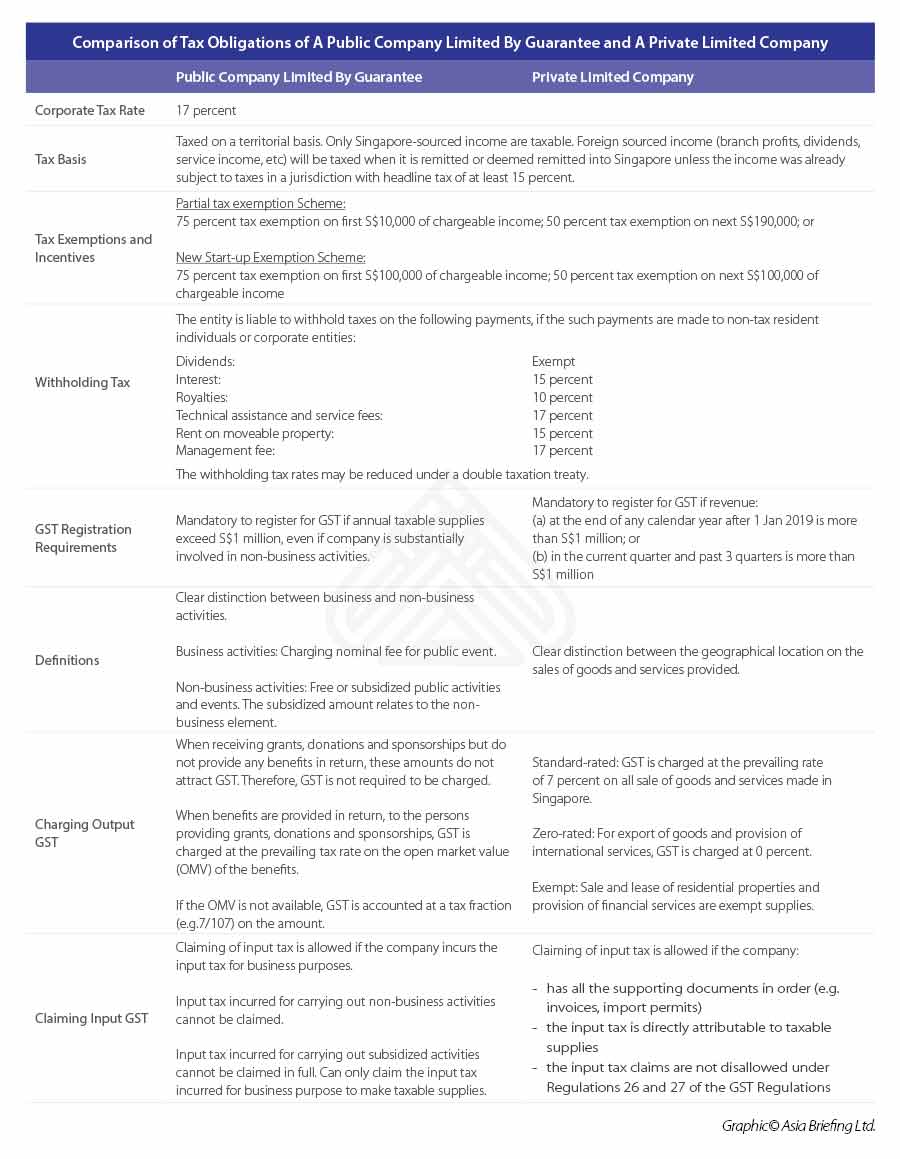

General tax exemptions for the Public Company Limited by Guarantee (PCLG) and the Society are the same. Both are exempt from income tax if 50 percent or less of the gross revenue are generated through its Singapore members that are entitled to tax-deduction.

If more, only the income generated by Singapore members will be subject to 17 percent corporate income tax. However, any income by non-members is subject to income tax irrespective of the above stated rules. The corporate tax rate is 17 percent unless granted charity status.

Tax obligations of a PCLG

The PCLG is the most popular form of establishing a NPO in Singapore as it entails a legal personality. A PCLG can benefit from the exemption scheme for new start-up companies. Established companies profit from 75 percent exemption for the first S$100,000 (US$72,000) and 50 percent for the subsequent S$200,000 (US$144,000). The law will be revised and companies established in or after 2020 will benefit only for the next S$100,000 (US$72,000).

Despite non-profit activities, if the annual taxable supply value of the charity exceeds or is expected to exceed S$1 million (US$ 720,000), the organization must register for Goods and Service Tax (GST). Grants, donations and sponsorships without benefits in return do not attract GST. The rates vary between zero percent and seven percent.

Taxable supplies by non-profits may, for example, be school fees, program fees and proceeds from the sale of donated goods. Exempted supplies could be interest received from bank deposits, proceeds from the sale of shares, bonds and unit trusts, rental income, and proceeds from the sale of residential properties.Paid input tax for non-business activities is normally unlikely as for business operations, non-refundable as the final supply is tax-exempted. However, there are two exceptions. First, input tax must not be paid if the sector is listed under regulations 33 of the GST Regulations. Second, under the de minimis rule, if the value of exempt supplies in any accounting period does not exceed S$40,000 (US$28,900) per month on average and five percent of the value of total supplies. If making payments to non-tax resident individuals or corporate entities, withholding tax applies. These rates may change under a double taxation agreement.

- Interests (15 percent);

- Royalties (10 percent);

- Payment for use of scientific or technical knowledge (10 percent);

- Rent on movable properties (15 percent);

- Technical assistance and service fee (17 percent); and

- Management fee (17 percent).

Additional tax benefits of a company limited by guarantee that carries on a trade or professional association

1. Satisfaction of 50 percent requirement

If more than 50 percent of its gross revenue receipts by way of entrance fees and subscriptions from Singapore members, the entity will not be deemed to be carrying on a business. The entity will only be liable to tax on income from other sources.

If less than 50 percent of its gross revenue is by way of entrance fees and subscriptions from Singapore members, the entity will be deemed to be carrying on a business. The entity will be taxed on operating surplus in addition to the income from other sources.

2. Requirements to be fulfilled

- It must be set-up for non-profit purposes, and if the company derives any surplus, it must be used to carry out its non-profit objectives;

- It exists for the sole purposes of benefiting its members and is operated exclusively for the same purpose for which it was organized;

- The contributors to the common fund, as a class, should be identical to the participators in the mutual surplus;

- There must be arrangements which entitle the contributors to the common fund to control it; and

- The constituent documents must prohibit the company limited by guarantee from making any distribution, whether in money, property or otherwise, to its members.

3. Application to enjoy tax treatment as a trade or professional association

In order to obtain approval to which the tax treatment above would be applicable, a company limited by guarantee that carries on a trade or professional association must make an application in writing to the Comptroller of Income Tax for such approval.

In the event the application is rejected, the entity will be taxed as per a Private Limited Company in Singapore. Third party service providers can provide assistance to companies that would like to apply for tax treatment as a trade or professional association as a public company limited by guarantee.

Charity status

In order to benefit from further tax incentives, a PCLG can apply to be treated under Charity status, which holds several advantages for non-profits. PCLGs as well as CTs, and Societies can apply for this special status within three months after their establishment through the Charity Portal. The charitable purposes can be classified as follows:

- The relief of poverty;

- The advancement of education;

- The advancement of religion; and

- Other purposes beneficial to the community.

Other purposes contain recognized reasons like the advancement of health, citizenship or community development, arts, heritage or science, environmental protection or improvement, relief to people in need or animal welfare.

When filing for recognition as a Charity the following provisions must be met in order to be eligible for the special status.

- The purposes are exclusively charitable;

- The organization has at least three governing board members, two of them Singapore citizens or permanent residents; and

- The purposes or objectives are wholly or substantially beneficial to the Singapore community.

Charities are exempt from property tax as well if the respective property is used for charitable purposes for social development in Singapore by approval of the Comptroller of Property Tax. However, the status does not come without strings attached. Charities must comply with specific rules guided by the Code of Governance to ensure the charitable purpose. They must:

- Submit financial statements and an annual report —

- audited for Charities with annual turnover of more than S$ 250,000,

- audited for PCLG’s as they fall under the Companies Act;

- Submit an annual report;

- Maintain accounting records for a minimum of five years; and

- Disclose fund-raising information online (when annual turnover exceeds S$ 500,000).

Institution of public character status

Organizations applying for the IPC scheme must already be approved as a Charity in Singapore. IPC status grants the organization permission to receive tax-deductible donations. It is exclusively granted to organizations that provide service to the community of Singapore as a whole without regard to race, creed, belief or religion.

Examples of entities that may be considered under the IPC scheme are:

- A non-profit hospital;

- Authority or society working or researching for the prevention or cure of disease of humans;

- Non-profit educational organizations;

- Public or private funds for scholarships;

- Non-profit organizations engaged or connected in the promotion of culture, arts or sports; and

- Other charities that are exclusively working for a charitable purpose.

When granted with IPC status, the compliance requirements for organizations increase as follows. The organization must in addition:

- Submit audited financial statements and an annual report;

- Issue tax deduction receipts to donors when receiving such donations;

- Maintain a donation record;

- Post financial and non-financial information online; and

- Submit a report on annual return on donations;

- Have an independent control body.

Tax deductible donations

Once registered as a charity under the IPC scheme, the relevant organization is eligible for tax deductible donations. Corporate and individual donors are allowed to donate cash to charities with IPC status and receive the tax exemption.

The donation, however, must have no commercial value, which is the case when the benefit is given in acknowledgement of the donation and has no resale value. Donations made to grant-making charities are tax-deductible as well.

Individual donors can donate shares. The value at the date when the share is legally received by the organizations counts, which makes donations of options and shares with restrictions on holding periods not eligible. Share donations to IPC’s are exempted from stamp duty.

Art donations by corporate or individual sponsors to a museum-approved with the National Heritage Board (NHB) are tax deductible. Artifact donations must be considered worthy for the collection by the NHB. Under the Public Art Tax Incentive Scheme (PATIS) money, sculptures or public artworks can be donated. The donor needs to apply to the NHB to assess the value of the donated sculpture or work of art.

Land and building donations are available for corporate and individual donors with tax exemption as well. After valuation by the revenue authority, the evaluated amount is eligible for a tax deduction. All donations to IPCs are exempted from stamp duty and estate duty.

Tax deduction of donations is currently set at 250 percent of the donated amount. Non-tax-deductible donations are for example ones where the donor is benefiting of the donation by displaying their banners or products at the event, facility or program by the receiving organization. Additionally, donations made for “foreign charitable purposes” are not tax deductible.

In general, non-profit organizations in Singapore benefit vastly from government incentives given even without special status. However, applying to become a charity is for any non-profit organization the right step for benefiting from major tax incentives.

With charity status, for example, the organization is automatically exempt from income tax payments. However, charities can apply to go under the IPC scheme as well which allows them to accept tax-deductible donations by individuals and corporate sponsors.

A version of this article appeared in the ASEAN Briefing magazine How to Set Up a Non-Profit Organization in Singapore.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City and Jakarta. Please contact us at asia@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Export Services in Indonesia: Eligible for Zero-Rated VAT

- Next Article Corporate Taxes in the Philippines