Singapore: Key Legislative Changes on AGMs and Annual Returns

With effect from August 31, 2018, changes to the Singapore compliance landscape have been introduced in a bid to uphold the country’s business-friendly reputation. The key legislative amendments are:

- Timeline alignments for holding Annual General Meetings (AGMs) and filing annual returns

- Exemption from holding AGMs for private companies

- Filing of simplified annual returns

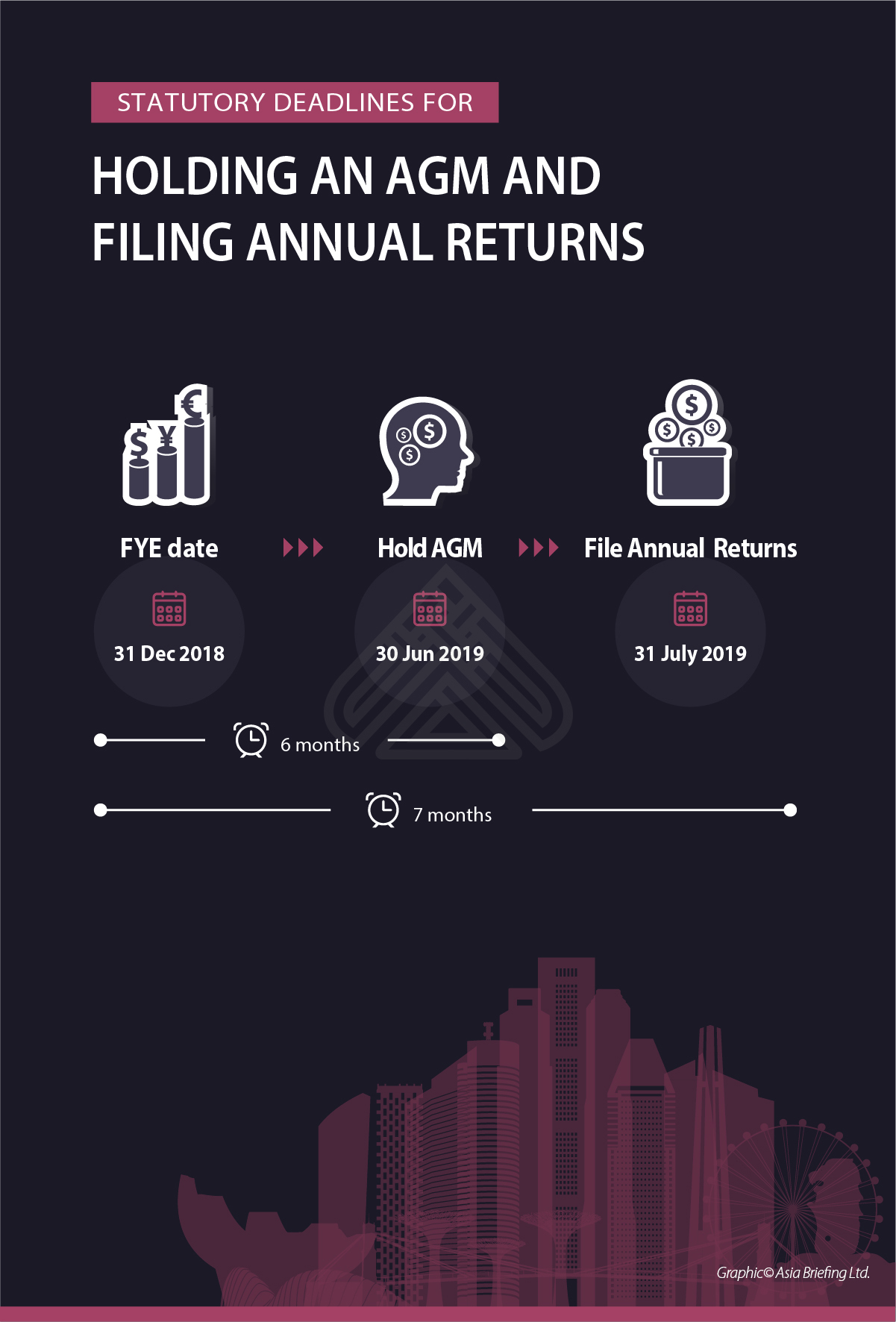

Timeline alignments for holding AGMs and filing of annual returns

Companies are now required to notify the Registrar on the financial year end (FYE) date.

With the new legislations in place, the statutory deadlines for holding an AGM and filing annual returns are illustrated below:

Important information on changing the FYE date:

- Companies must notify the Registrar of their FYE date upon incorporation and of any subsequent change;

- Companies must apply to the Registrar for approval to change their FYE date if the change in FYE results in a financial period exceeding 18 months; or if the FYE was changed within the last 5 years;

- Duration of financial year must not exceed 18 months in the year of incorporation

- Only FYE of the current and immediate preceding financial year may be changed if statutory deadlines for AGM, annual returns and sending of financial statements have not passed

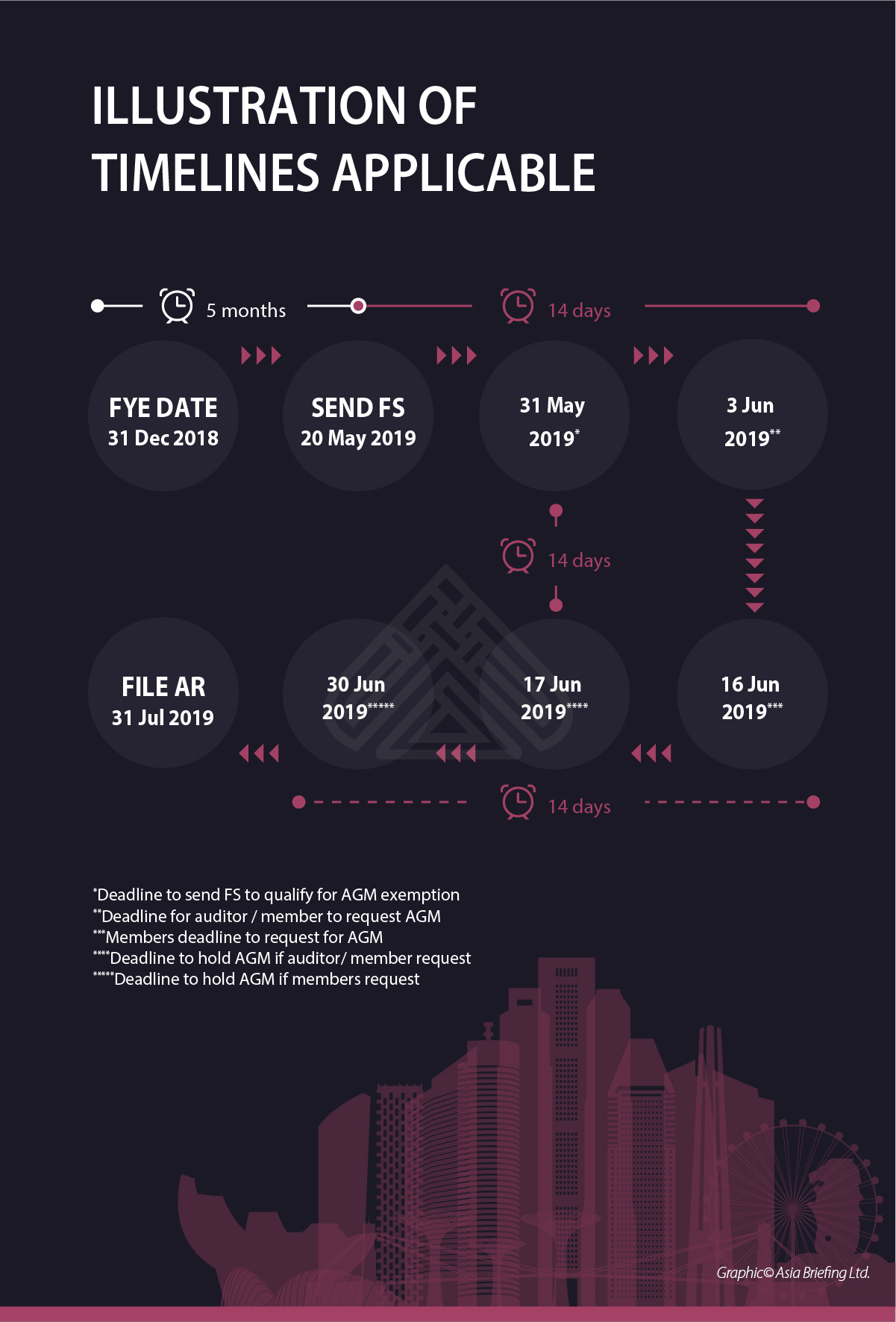

Exemption from holding AGMs for private companies

The AGM exemption applies to private companies if financial statements are sent to members (i.e. shareholders) within 5 months after the FYE and all members approve a resolution to dispense with the holding of AGM.

Private dormant companies exempt from the preparation of financial statements are not required to hold an AGM, subject to the safeguards mentioned below.

Safeguards prescribed by the Companies (Amendment) Act 2017:

- Any member requesting for an AGM shall notify the company not later than 14 days before the last 6th month after the FYE date;

- If the company is notified of such request, directors must hold an AGM within 6 months after the FYE date. The company may seek for the Registrar’s approval for an extension of time if required.

- If any member or auditor requests for an AGM not later than 14 days after the financial statements are sent out, directors must hold an AGM within 14 days after the date of request.

Filing of simplified annual returns

Companies with FYE dates ending on or after August 31, 2018 and declaring as “Solvent Exempt Private Company” or “Private Dormant Relevant Company” will be eligible to lodge a Simplified Annual Returns if the following requirements are met:

- the company is not preparing audited financial statements; and

- the company is not required to file financial statements

Simplified Annual Returns can only be filed if:

- after the AGM has been held (if the company is required to hold an AGM); or

- after financial statements have been sent to members (if the company is not required to hold an AGM); or

- after the FYE date for a private dormant relevant company exempted from preparing financial statements

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City and Jakarta. Please contact us at asia@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Indonesia Eases Tax Holiday Policy for New FDI Projects in All Sectors

- Next Article Bank Indonesia to Standardize QR Code Payment