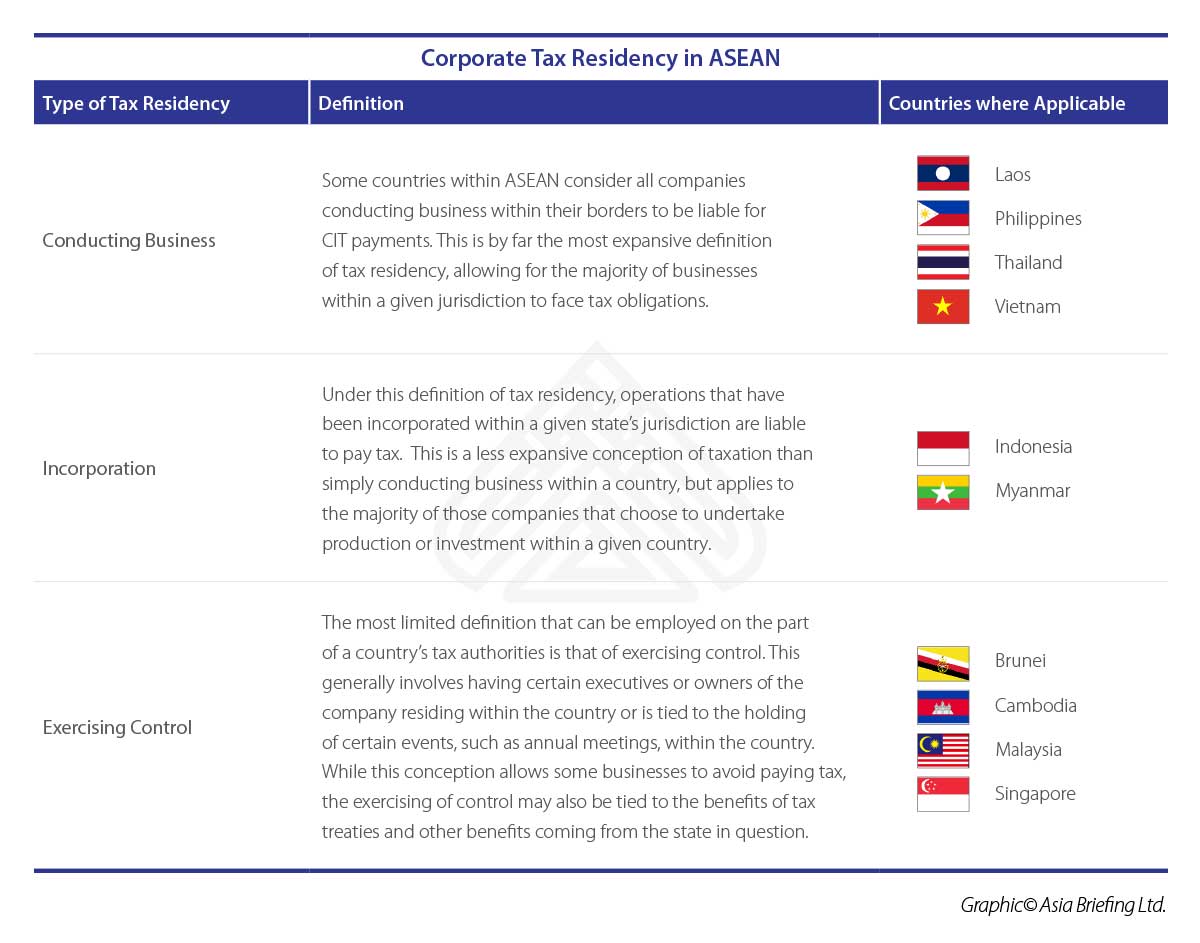

Taxation in ASEAN: An Introduction

The Association of Southeast Asian Nations (ASEAN) represents a highly integrated economic region when compared to other parts of the world. Yet, in terms of taxation, there is a wide variation among its 10 member states namely, Brunei, Laos, Cambodia, Indonesia, Myanmar, Malaysia, Philippines, Singapore, Thailand, and Vietnam. Apart from the reduction of import tariffs, ASEAN tax coordination is limited to the elimination of certain withholding taxes and the completion of the network of double tax treaties among all ASEAN countries. Companies that are looking to enter emerging markets in ASEAN must take note of the various taxes they may be subject to, and their variation across the region. Applicable taxes for foreign businesses include Corporate Income Tax (CIT), Personal Income Tax (PIT), Withholding Tax, as well as indirect taxes such as Value Added Tax (VAT), and Goods and Services Tax (GST). The impact of the different taxes, tax rates and tax bases on the effective tax burdens, however, may differ according to the type of investment, the source of finance and the profitability of an investment.

![]() RELATED: Tax Services from Dezan Shira & Associates

RELATED: Tax Services from Dezan Shira & Associates

Personal Income Tax

PIT is levied on income or profitable income of all individuals in a given jurisdiction. In the ASEAN region, all countries except Brunei and Cambodia employ a progressive PIT system wherein the tax rate levied increases in proportion to the increase in taxable income. As a result, individuals with high taxable income are taxed proportionately more than those with lower income. PIT rates vary across the ASEAN region, with some member countries capping their maximum PIT at as much as 35 percent and others at as little as 20 percent.

VAT & GST

Indirect taxes are levied at every level of production of a good and service and are generally included in the price of the product. Such taxes add to the cost of a purchasable product and are less obvious to consumers than other forms of taxes such as the CIT or the PIT; both of which require a business or an individual to pay the accruing tax directly to a government.

In ASEAN, most popular forms of indirect taxation are GST and VAT. Though countries such as Brunei do not impose indirect taxes at all. We have compared indirect taxes across ASEAN in the next chapter.

Withholding Tax

Withholding tax is a tax levied at source on individuals or companies making a payment to any non-resident entity. Usually, the percentage of the tax rates vary considerably depending on the tax subject, and the agreements signed between the governments of the parties involved in the transaction. In ASEAN, withholding tax is widely used in the form of dividends, interests and royalties payments.

Dividends: For the majority of foreign-owned enterprises, dividends form the primary means of repatriating profits from their ASEAN based operations. Dividends are in essence the compensation of shareholders (corporate or individual) derived from the business performance of the enterprise in which they have a financial interest.

Royalties: In some cases, companies may lease patents, designs, or other physical assets to their operations in ASEAN. Royalty payments include all outgoing profits tied to the payment for the retention of these assets.

Interest: Interest is generally used in the event that project financing is achieved through a decree of financial leveraging. Interest payments are all outgoing funds used to service existing financial obligations.

Corporate Income Tax

CIT is a direct tax levied by a jurisdiction on a company’s income or the chargeable gains accruing to companies. In ASEAN, every country imposes a varying rate of CIT, with some jurisdictions fixing it at as high as 30 percent and others at a comparatively low rate of 17 percent. The rate is determined by a myriad of factors including the priorities of government (whether more emphasis is placed on state revenue or investment), the nature of its economy (how reliant it is on foreign investment), the country’s size, and its level of development.

The definition of what a corporation is and whether it is subject to CIT varies from country to country. While the specifics of each country’s policies with regard to taxation should be monitored closely, tax residency can roughly be divided into the following three categories of treatment:

This article is an excerpt from the March 2018 issue of ASEAN Briefing magazine, titled “The 2018/19 ASEAN Tax Comparator“. In this issue, we discuss both the continuity and change in ASEAN’s tax landscape and what it means for foreign investors. We begin by highlighting the salient features of the taxation regimes of the individual member states of ASEAN. We examine the various forms of taxation within ASEAN while highlighting their regional variations. We then provide an inter-country comparison of tax rates, including in relation to PIT, CIT, VAT and GST, which is essential for making informed FDI decisions. Finally, we analyze the ease or burden of tax compliance in ASEAN in 2018 and beyond.

This article is an excerpt from the March 2018 issue of ASEAN Briefing magazine, titled “The 2018/19 ASEAN Tax Comparator“. In this issue, we discuss both the continuity and change in ASEAN’s tax landscape and what it means for foreign investors. We begin by highlighting the salient features of the taxation regimes of the individual member states of ASEAN. We examine the various forms of taxation within ASEAN while highlighting their regional variations. We then provide an inter-country comparison of tax rates, including in relation to PIT, CIT, VAT and GST, which is essential for making informed FDI decisions. Finally, we analyze the ease or burden of tax compliance in ASEAN in 2018 and beyond.

About Us

ASEAN Briefing is produced by Dezan Shira & Associates. The firm assists foreign investors throughout Asia and maintains offices throughout ASEAN, including in Singapore, Hanoi, Ho Chi Minh City and Jakarta. Please contact us at asia@dezshira.com or visit our website at www.dezshira.com.

- Previous Article Design Rights Protection in South East Asia

- Next Article IP Protection in Indonesia’s Food and Beverage Industry