Understanding Inheritance and Estate Tax in ASEAN

Inheritance and estate taxes (sometimes referred to as “death taxes”) can have a significant financial effect upon your assets if you are not ready for their imposition. While ASEAN is working to standardize many financial regulations throughout the economic community, inheritance and estate taxes are still imposed differently depending on the country.

An estate tax collects tax calculated on the net value of the deceased’s overall property, while an inheritance tax is calculated on the inheritance received by individuals.

Below we provide a snapshot into the current and future regulations relating to these types of taxes in the ASEAN member nations.

Singapore:

Before 2008, Singapore levied a tax called the “Estate Duty”, however, this was removed in order to encourage more local and overseas investors to hold their assets in the city-state.

Before the abolition of the Estate Duty, immovable property, bank accounts, publicly listed shares and items in a safe deposit box were all taxable.

![]() RELATED: Tax Exemptions on Foreign Income for Singapore- Based Companies

RELATED: Tax Exemptions on Foreign Income for Singapore- Based Companies

The Philippines:

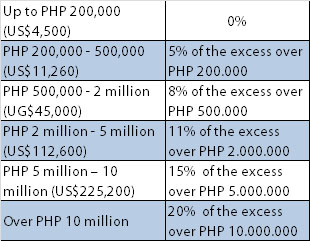

Currently, the Philippines have an estate tax in place. After deducting all expenses, losses, debts and taxes related to the property, the taxable inheritance amount is arrived at.

Nonresident foreigners are only liable to estate tax for property located within the territory of the Philippines. The following deductions are available for citizens and resident foreigners, before arriving at the taxable threshold:

- PHP 1 million (US$22,500) “standard” deduction

- PHP 1 million for the family home

- PHP 200,000 (US$4,500) for expenses relating to the funeral

- PHP 500,000 (US$11,260) for medical expenses that occurred in the year before the deceased’s death

Similar to Vietnam, there are “compulsory heirs” in the Philippines. Depending on the heirs’ relationship to the deceased person, at least one half of the hereditary estate is reserved for distribution between the heirs. The hereditary estate is the difference between the assets and the liabilities of the deceased.

All property, which the deceased gifted during his lifetime will be regarded as an advance from his estate – and labeled collation. The value of that property will be included in the hereditary estate. Even if the property was gifted upon birth of the heirs, the law will still regard that as collation. Of course, this will only apply to gifts of great value (real estate, cars, stocks, jewelry, etc.).

The “compulsory heir rule” does not apply to foreigners. However, in some cases (e.g. foreigners owning property in the Philippines) inheritance issues of expatriates might become subject to renvoi, meaning that these issues are referred back to the Philippines.

![]() RELATED: Dezan Shira & Associates’ Tax and Compliance Services

RELATED: Dezan Shira & Associates’ Tax and Compliance Services

Indonesia:

Indonesia does not levy inheritance tax. As long as there is no business or employment relationship, there is also no gift tax.

However, if real estate is transferred after the death of a proprietary, a real estate transfer tax can be levied.

Vietnam:

Any inherited property exceeding VND10 million (US$460,000) is taxed at a flat rate of 10 percent. However, exemptions from inheritance tax are made if the income is generated from the inheritance of real property as long as one of the following relationships is applicable to the heir and the deceased person: husband and wife; parent and child, including adopted children and foster parents; Mother and father-in-law, Child-in-law; Grandparent and Grandchild; Sibling.

Since in the Socialist Republic of Vietnam land belongs to the Vietnamese people as a whole, real estate property cannot be inherited, but the right to use these lands can be. Only Vietnamese nationals can be legal owners of immovable property, meaning that immovable property must be sold and foreign beneficiaries can only inherit the amount equal to the value of the property.

Certain persons (ex. convicts, persons breaching their duty to support the deceased, and persons forcing the deceased to include them in their will) are not allowed to inherit. In Vietnam, the rule of compulsory heirs is also applicable, meaning that minor children, fathers, mothers, spouses, and adult children who are incapable of working will inherit shares of the bequeathed property, regardless of the content of will.

Malaysia:

Inheritance tax in Malaysia was abolished in 1991. Until then, net worth exceeding MYR2 million (US$543,000) was taxed at five per cent, and a rate of 10 percent was imposed on net worth exceeding MYR 4 million.

Thailand:

In August 2014, the head of Thailand’s National Council for Peace and Order (NCPO), General Prayuth Chan-ocha approved plans to reform the tax system – which included the creation of an inheritance tax. The 10 percent tax will be levied on values over the amount of US$ 1.5 million, effectively making this a wealth distribution tax.

![]() RELATED: Thailand considers inheritance tax

RELATED: Thailand considers inheritance tax

Brunei:

In the Sultanate, estate duty is payable and applied to all immovable property located in Brunei and movable property outside of the country, exceeding the accumulated amount of B$2 million (US$1.4 million). The tax rate is currently set at three per cent.

Cambodia:

No inheritance or estate tax is levied in Cambodia. Legally speaking, foreigners are not allowed to inherit in Cambodia, and must first apply for citizenship if they want to qualify. However, one strategy to circumvent this problem is by holding the property through a resident company.

Lao PDR and Myanmar:

Neither Laos nor Myanmar levies inheritance taxes. However, in the case of Myanmar, inheritances and gifts are subject to stamp duty.

|

Asia Briefing Ltd. is a subsidiary of Dezan Shira & Associates. Dezan Shira is a specialist foreign direct investment practice, providing corporate establishment, business advisory, tax advisory and compliance, accounting, payroll, due diligence and financial review services to multinationals investing in China, Hong Kong, India, Vietnam, Singapore and the rest of ASEAN. For further information, please email asean@dezshira.com or visit www.dezshira.com. Stay up to date with the latest business and investment trends in Asia by subscribing to our complimentary update service featuring news, commentary and regulatory insight. |

![]()

Tax, Accounting, and Audit in Vietnam 2014-2015

Tax, Accounting, and Audit in Vietnam 2014-2015

The first edition of Tax, Accounting, and Audit in Vietnam, published in 2014, offers a comprehensive overview of the major taxes foreign investors are likely to encounter when establishing or operating a business in Vietnam, as well as other tax-relevant obligations. This concise, detailed, yet pragmatic guide is ideal for CFOs, compliance officers and heads of accounting who need to be able to navigate the complex tax and accounting landscape in Vietnam in order to effectively manage and strategically plan their Vietnam operations.

An Introduction to Tax Treaties Throughout Asia

An Introduction to Tax Treaties Throughout Asia

In this issue of Asia Briefing Magazine, we take a look at the various types of trade and tax treaties that exist between Asian nations. These include bilateral investment treaties, double tax treaties and free trade agreements – all of which directly affect businesses operating in Asia.

The 2014 Asia Tax Comparator

The 2014 Asia Tax Comparator

In this issue of Asia Briefing Magazine, we examine the different tax rates in 13 Asian jurisdictions – the 10 countries of ASEAN, plus China, India and Hong Kong. We examine the on-the-ground tax rates that each of these countries levy, including corporate income tax, individual income tax, indirect tax and withholding tax. We also examine residency triggers, as well as available tax incentives for the foreign investor and important com

- Previous Article British Firms Encouraged to Expand into the Philippines

- Next Article ASEAN Case Study: The Auto Industry and GM